New data out today reveals that prices for petrol vary significantly by retailer, with Coles Express the most expensive on average across the five main capital cities, and Woolworths and independents generally the cheapest, meaning consumers who switch brands can save significant dollars.

The ACCC’s in-depth petrol report details annual average retail petrol prices throughout 2017 and identifies the highest and lowest priced major retailers in Sydney, Melbourne, Brisbane, Adelaide and Perth.

The difference in prices on average across retailers ranged from 9.5 cents per litre recorded in Sydney to 3.6 cents per litre in Melbourne in 2017.

"Our analysis of petrol prices shows the range between major retailers with the highest average price and lowest average price varied across each city considerably," ACCC Chairman Rod Sims said.

"Independent chains were the lowest priced in each of the five major cities and Woolworths was generally below the market average price in most cities. Average prices at Coles Express were the highest in all five cities, and average prices at retail sites where BP and Caltex head office sets the retail price were generally above the market average price."

"The majority of consumers tend to go to the same petrol station every time they fill up. This research shows it might be time to consider which station to fill up at," Mr Sims said.

The report also examined the difference between average prices in 2017 with those in 2007. It found the range between major retailers charging the highest average price and those charging the lowest average price had increased significantly since 2007.

The average prices of BP-branded retail sites were above the market average price in all five cities in 2007 and 2017. The average price of Caltex-branded sites were above the market average in the majority of the five cities in the two periods.

"What this analysis tells us is the decision about which retailer to buy petrol from is even more important in 2017 than it was in 2007. Retailers’ prices are not the same, they price differently and have different strategies to get you to fill up with them," Mr Sims said.

"We want to remind drivers there are plenty of apps they can download for free that will tell them where to buy the cheapest petrol in their area. Many people are paying more than they need to for petrol."

"Shopping around has the added benefit of increasing competition by putting pressure on retailers who charge the most to lower their prices or risk losing customers," Mr Sims said.

There are a variety of fuel price websites and apps that provide information to drivers about petrol prices, including: the NSW FuelCheck website and app, the Northern Territory MyFuel NT website and app, the WA FuelWatch website, the MotorMouth website and app, and apps operated by GasBuddy, the NRMA, 7-Eleven and Woolworths. The Queensland Government recently announced it would commence a two-year trial that requires fuel retailers to collate and publish their latest prices online.

Background

On 20 December 2017, the Treasurer directed the ACCC to monitor the prices, costs and profits relating to the supply of petroleum products and related services in Australia. See: ACCC's fuel monitoring role

Under this direction, the ACCC produces quarterly petrol monitoring reports focusing on the price movements in the capital cities and over 190 regional locations across Australia. It also produces industry reports that focus on particular aspects of consumer interest in the fuel market. This is the first of those reports.

Regular unleaded petrol (RULP) prices were analysed in Melbourne, Brisbane, Adelaide and Perth, and E10 (i.e. RULP with up to 10 per cent ethanol) prices were analysed in Sydney. All prices are board prices and do not take account of the various discount schemes.

In this analysis a major retailer is defined as a retailer that sets petrol prices at 10 or more retail sites in the city.

While the brand of the retail site will often reflect the owner or price setter of the retail site, this is not always the case. For example, there are BP- and Caltex-branded but independently operated retail sites where the independent operator sets the price. These sites differ from company-owned and company-operated and commission agent sites (referred to as COCO sites), where BP and Caltex head office set the price.

This analysis focused on the five largest cities because they generally have a larger range of prices, and more retail sites, than the smaller capital cities (i.e. Canberra, Hobart and Darwin) and regional locations across Australia.

The charts below show the difference between each major retailer’s annual average petrol price and the market annual average petrol price in each of the five cities in 2017. It also shows the proportion of retail sites in the city for each major retailer as at 30 June 2017, which provides an indication of the significance of each major retailer’s prices in the market.

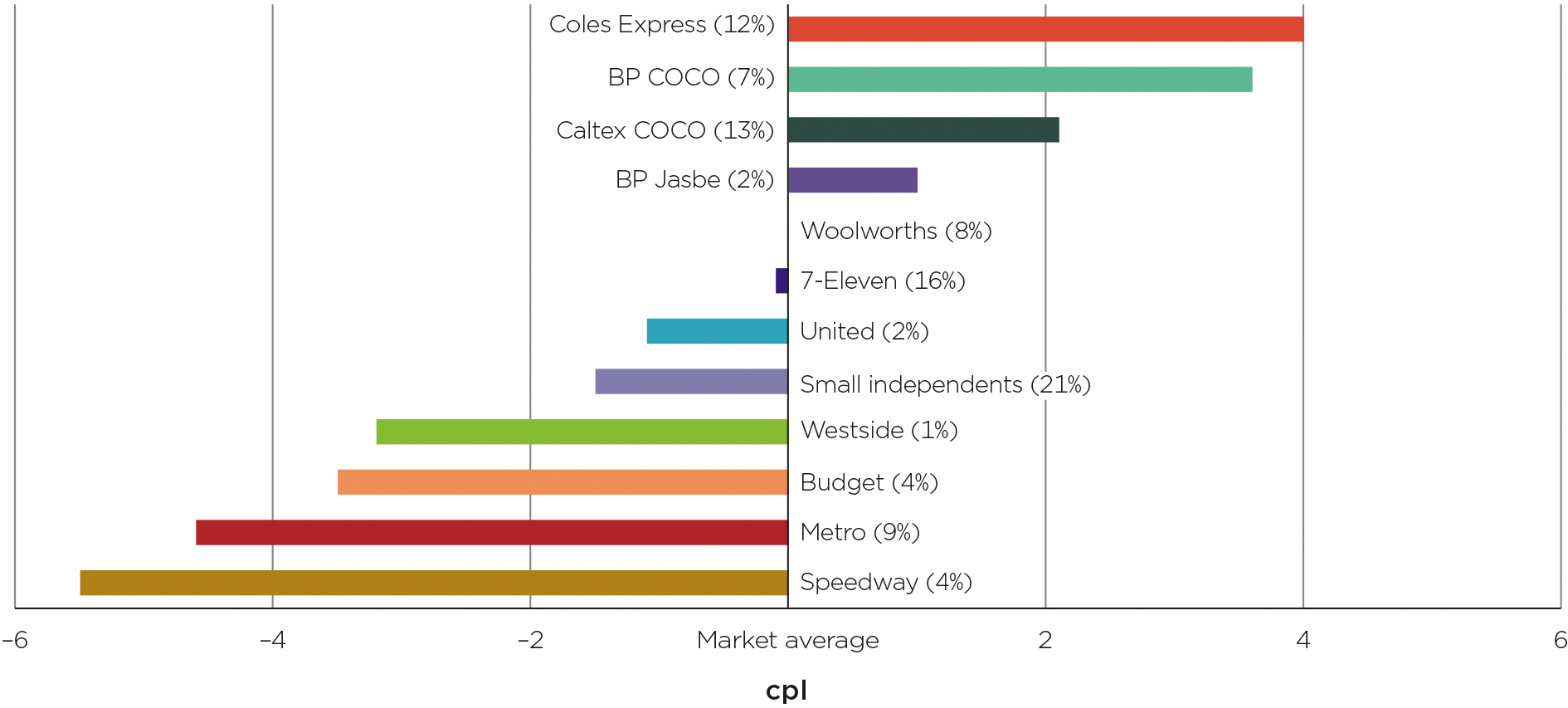

Difference between each major retailer’s annual average E10 price and the market annual average E10 price in Sydney in 2017

Source: ACCC calculations based on Informed Sources data and information provided by some major retailers.

Notes: The number in brackets for each major retailer is the proportion of retail sites in the city for that retailer. The proportions of retail sites shown in the chart do not total 100 per cent due to rounding. The annual average Woolworths price was equal to the market average price. BP Jasbe is a BP-branded independent chain.

The average prices of six major retailers (Speedway, Metro, Budget, Westside, United and 7-Eleven) and the ‘small independents’ category were below the market average price (124.5 cpl). The average price of one retailer (Woolworths) was equal to the market average price. These retailers account for around 65 per cent of the total number of retail sites in Sydney.

The average prices of four major retailers (Coles Express, BP COCO, Caltex COCO and BP Jasbe) were above the market average price. These retailers account for around 34 per cent of the total number of retail sites in Sydney.

Speedway’s average price was the lowest, at 5.5 cpl below the market average price, and Coles Express’ average price was the highest, at 4.0 cpl above the market average price. There was a range of 9.5 cpl between the lowest and the highest priced retailers.

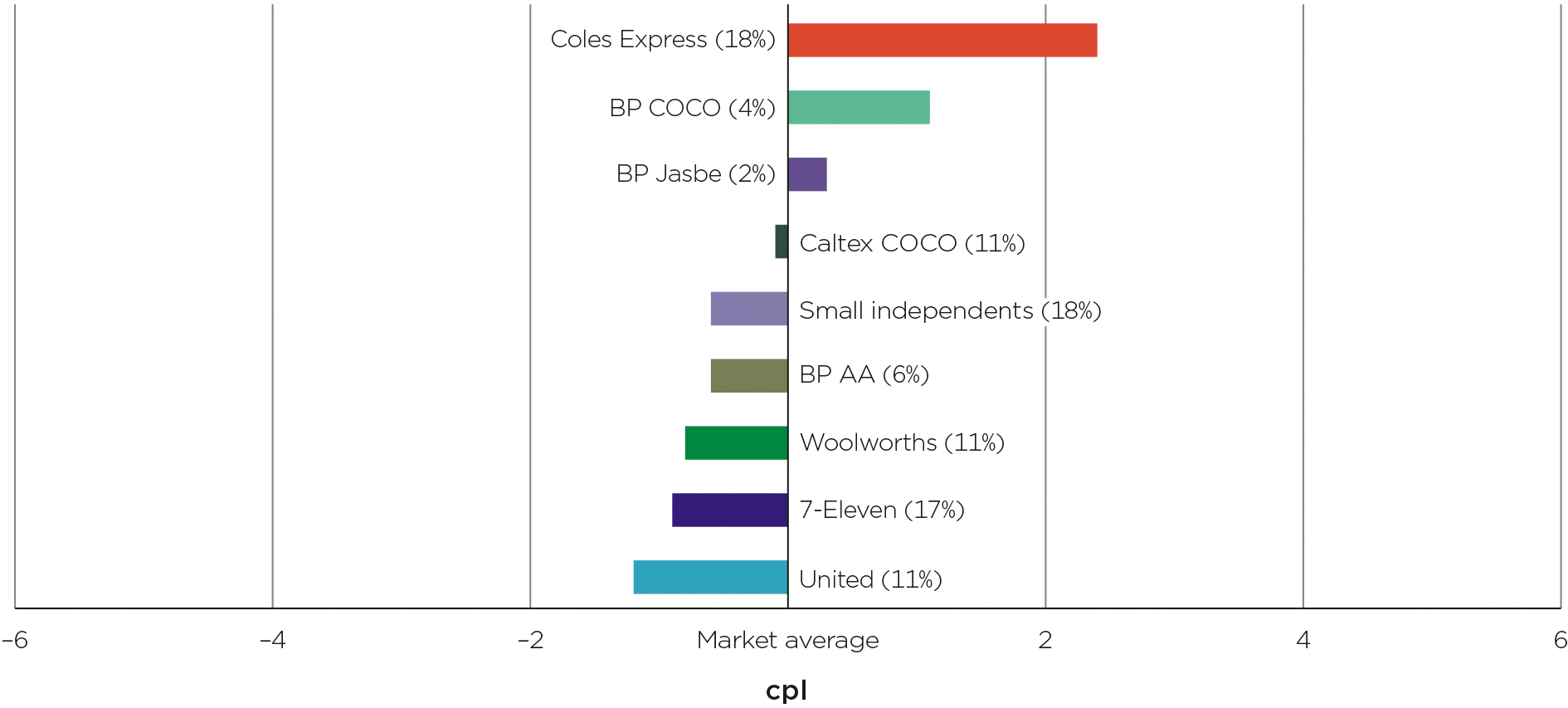

Difference between each major retailer’s annual average RULP price and the market annual average RULP price in Melbourne in 2017

Source: ACCC calculations based on Informed Sources data and information provided by some major retailers.

Notes: The number in brackets for each major retailer is the proportion of retail sites in the city for each major retailer. Prices were unavailable for Liberty retail sites in Melbourne. Therefore, the proportions of retail sites shown in the chart do not total 100 per cent. BP Jasbe and BP AA are BP-branded independent chains.

The average prices of five major retailers (United, 7-Eleven, Woolworths, BP AA and Caltex COCO) and the ‘small independents’ category were below the market average price (128.8 cpl). These retailers account for around 74 per cent of the total number of retail sites in Melbourne.

The average prices of three major retailers (Coles Express, BP COCO and BP Jasbe) were above the market average price. These retailers account for around 24 per cent of the total number of retail sites in Melbourne.

United’s average price was the lowest, at 1.2 cpl below the market average price, and Coles Express’ average price was the highest, at 2.4 cpl above the market average price. There was a range of 3.6 cpl between the lowest and the highest priced retailers.

Difference between each major retailer’s annual average RULP price and the market annual average RULP price in Brisbane in 2017

Source: ACCC calculations based on Informed Sources data and information provided by some major retailers.

Note: The numbers in brackets are the proportion of retail sites in the city for each major retailer.

The average prices of four major retailers (United, 7-Eleven, Puma Energy and Woolworths) and the ‘small independents’ category were below the market average price (130.0 cpl). These retailers account for around 59 per cent of the total number of retail sites in Brisbane.

The average prices of four major retailers (Coles Express, BP COCO, Freedom Fuels and Caltex COCO) were above the market average price. These retailers account for around 41 per cent of the total number of retail sites in Brisbane.

United’s average price was the lowest, at 3.3 cpl below the market average price and Coles Express’ average price was the highest, at 3.1 cpl above the market average price. There was a range of 6.4 cpl between the lowest and the highest priced retailers.

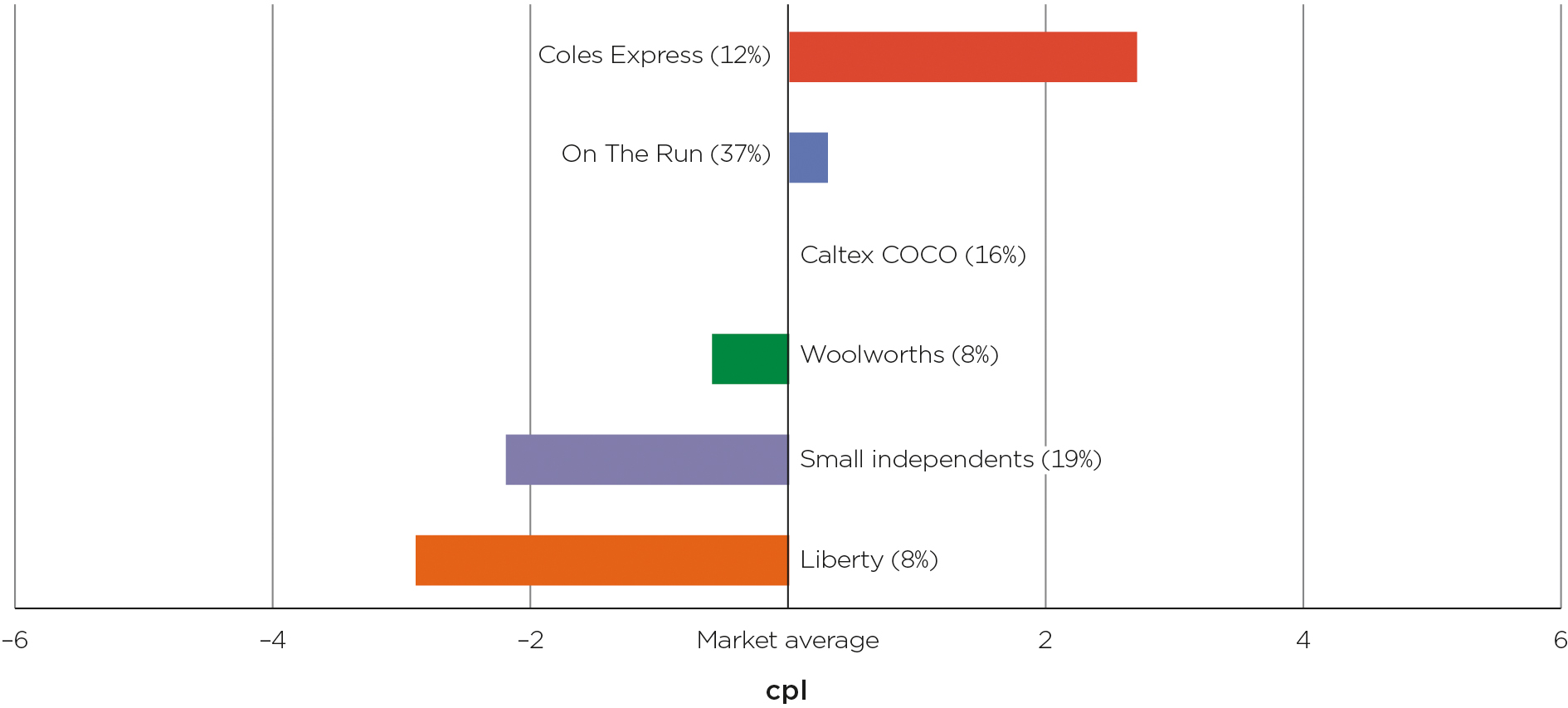

Difference between each major retailer’s annual average RULP price and the market annual average RULP price in Adelaide in 2017

Source: ACCC calculations based on Informed Sources data and information provided by some major retailers.

Notes: The numbers in brackets are the proportion of retail sites in the city for each major retailer. The annual average Caltex COCO price was equal to the market average price.

The average prices of Liberty and Woolworths, and the ‘small independents’ category, were below the market average price (126.3 cpl), and average prices of one retailer (Caltex COCO) were equal to the market average price. These retailers account for around 51 per cent of the total number of retail sites in Adelaide.

The average prices of Coles Express and On The Run were above the market average price. These retailers account for around 49 per cent of the total number of retail sites in Adelaide.

Liberty’s average price was the lowest, at 2.9 cpl below the market average price and Coles Express’ average price was the highest, at 2.7 cpl above the market average price. There was a range of 5.6 cpl between the lowest and the highest priced retailers.

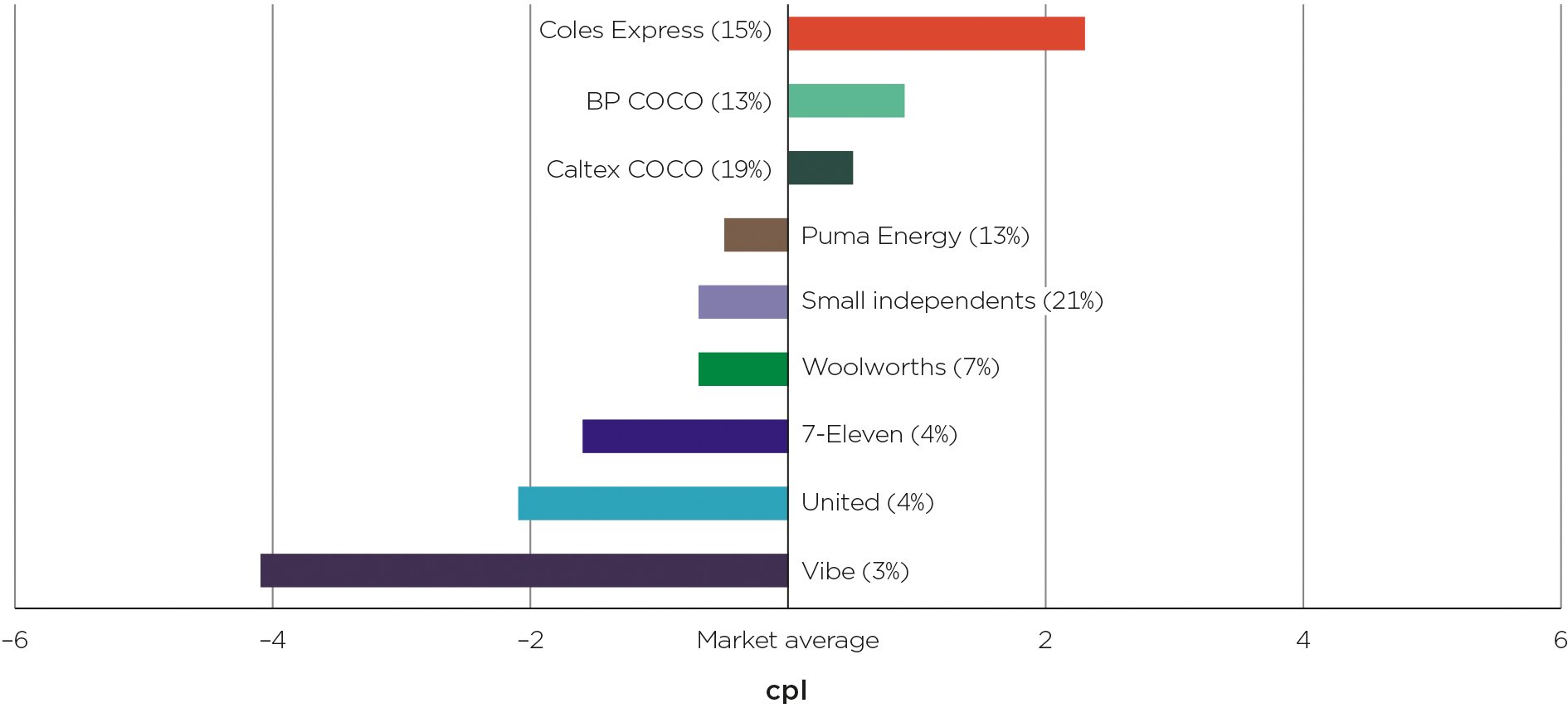

Difference between each major retailer’s annual average RULP price and the market annual average RULP price in Perth in 2017

Source: ACCC calculations based on Informed Sources data and information provided by some major retailers.

Notes: The numbers in brackets are the proportion of retail sites in the city for each major retailer. The proportions of retail sites shown in the chart do not total 100 per cent due to rounding.

The average prices of five major retailers (Vibe, United, 7-Eleven, Woolworths and Puma Energy) and the ‘small independents’ category were below the market average price (128.5 cpl). These retailers account for around 52 per cent of the total number of retail sites in Perth.

The average prices of three major retailers (Coles Express, BP COCO and Caltex COCO) were above the market average price. These retailers account for around 47 per cent of the total number of retail sites in Perth.

Vibe’s average price was the lowest in Perth, at 4.1 cpl below the market average price and Coles Express’ average price was the highest, at 2.3 cpl above the market average price. There was a range of 6.4 cpl between the lowest and the highest priced retailers.