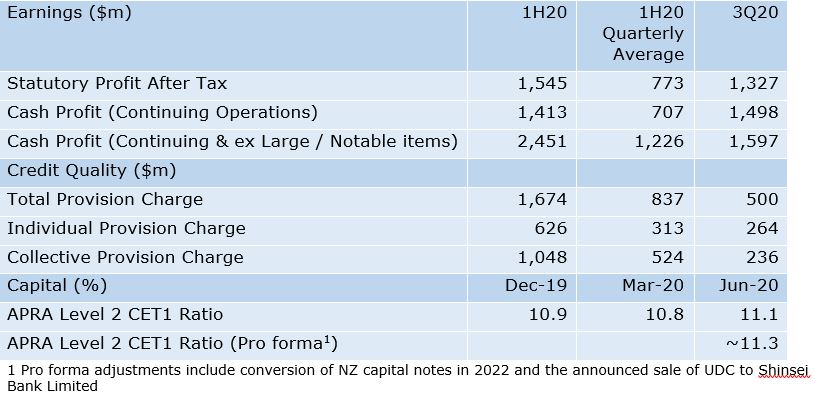

ANZ today announced an unaudited statutory profit for the third quarter to 30 June 2020 of $1,327 million with an unaudited cash profit from continuing operations of $1,498 million.

Following the deferral of a decision on the interim dividend in April 2020, ANZ's Board also proposed an interim dividend of 25 cents per-share, fully franked.

FINANCIAL PERFORMANCE SUMMARY

CEO COMMENTARY

ANZ Chief Executive Shayne Elliott said: "Our performance during these difficult times demonstrates the strength of our portfolio as we balance the need to support customers and our staff through this global pandemic while also providing a fair return for shareholders.

"Our company purpose of helping people and communities thrive has guided our response. Challenges clearly still remain, however having moved quickly to protecting the things that matter, engaging with key stakeholders, adapting for a new world, while also preparing for the future has us well placed.

"I'm proud of how our people have worked hard to not only support our customers but also the broader economy. We will continue to do what we can to help customers get back on track as this is ultimately in the long-term interests of our stakeholders, including shareholders. We will maintain our close engagement with Government and regulators who have played a critical role in softening the economic impact of this virus.

"During the quarter we have grown home loans in Australia well above the rest of the market. We are also pleased with the strong deposit growth, demonstrating customers are taking a prudent approach in shoring up their personal finances.

"As a result of strong customer flows and underlying volatility, our markets business was up 60% on the first half quarterly average, while a reduction in risk weighted assets from our International business also delivered a capital benefit to the Group.

"We continued the simplification of our business with the announced sale of UDC in New Zealand to Shinsei Bank and an agreement to sell our off-site ATM fleet in Australia to Armaguard.

"We are better placed than when we went into the GFC with investments in data analytics and real-time monitoring systems allowing us to spot trends quickly and respond to our customers' needs promptly.

"You only need to look at the reintroduction of community lockdowns in Victoria and Auckland to realise we all still have a way to go before this virus is behind us. There will be more challenges along the way, however I'm confident Australia, New Zealand and the key Asian countries where we operate are well placed to lead a global economic recovery," Mr Elliott said.

DIVIDEND & CAPITAL

ANZ announced today that the Board proposes a 2020 interim dividend which will see a fully-franked (for Australian tax purposes) distribution of 25 cents per share paid to shareholders on 30 September 2020. New Zealand imputation credits of NZ$ 3 cents per ordinary share will also be attached.

This decision took into account ANZ's continuing capital strength and the updated regulatory guidance, while also balancing shareholder needs with the uncertain future impact of COVID-19.

The record date for determining entitlements to the proposed 2020 interim dividend will be 25 August 2020. The Dividend Reinvestment Plan (DRP) and Bonus Option Plan (BOP) will continue to operate in respect of the 2020 interim dividend without a discount and key dates and associated information in relation to the dividend, DRP and BOP will be provided separately.

The interim dividend represents 46% of ANZ's 1H20 statutory profit, or 30% of 1H20 statutory profit adjusted for the impairment of Asian associates at 31 March, which reduced statutory profit but did not impact capital as the investments are full capital deductions.

ANZ Chairman David Gonski said: "We know many of our shareholders rely on dividends. We've been able to build on our strong capital position this quarter, and this has enabled us to pay a dividend that balances the needs of our shareholders with the uncertain economic environment. We agree with APRA's view that all ADIs should be prudent in considering dividends. We arrived at our decision independently and it sits comfortably within APRA's guidance."

The Group's capital position continues to be strong, allowing ANZ to play a role in supporting the recovery, with a Level 2 Common Equity Tier 1 capital (CET1) ratio of 11.1% at 30 June 2020. The CET1 ratio increased 37 basis points from March and benefitted from an $10 billion reduction in credit risk weighted assets in Institutional (excluding the impacts of exchange rates and risk migration), mainly within the International business.

The Group's pro forma CET1 ratio was 11.3% and includes the conversion of the NZ$ capital notes in 2022 and the announced sale of UDC to Shinsei Bank Limited, expected to complete in the coming weeks.

COVID-19 SUPPORT

ANZ launched support packages for retail and commercial customers in Australia and New Zealand that included the option of an up to six-month loan repayment deferral. ANZ is continuing to work with customers impacted by COVID-19 to restructure loans and in some circumstances will provide an extension to loan repayment deferrals for a further four months.

In Australia, ANZ has ~84,000 deferrals in place for home loan accounts at 31 July 2020 valued at $31 billion, representing 9% of Australian home loan accounts. ANZ has deferred ~22,000 business loans at 31 July 2020 valued at $9.5 billion, representing ~14% of commercial lending exposures. Approval processes for key government initiatives such as JobKeeper and the SME Loan Guarantee were streamlined during the quarter.

In New Zealand, ANZ provided support to ~39,000 customers which included deferrals on 24,000 home loans valued at NZ$6 billion, representing ~6% of New Zealand's Home Loan portfolio. ANZ also granted ~2,700 temporary overdraft facilities to businesses needing more working capital.

CREDIT QUALITY

The total provision charge in the June quarter was $500 million, and follows the $1,674 million taken at the first half. This new charge includes an individually assessed provision charge of $264 million and a collective provision charge of $236 million as we strengthened credit reserves, in particular for deferral packages and our small business customers. The collective provision (CP) balance increased to $4,648 million as at 30 June 2020 with a coverage ratio (CP Balance / Credit RWA) of 1.25%, up from 0.75% prior to the adoption of AASB 9 in September 2018.

An interview with Chief Executive Officer Shayne Elliott discussing the trading update can be found at bluenotes.anz.com