The February 2026 edition of the APEC Regional Trends Analysis (ARTA) points to a cautiously improved outlook for the Asia‑Pacific region. Growth momentum has strengthened, supported by resilient consumption, robust trade performance and a surge in AI‑related investment. Yet even as near-term prospects brighten, the report underscores that underlying vulnerabilities are deepening, leaving policymakers with the challenge of sustaining momentum while managing rising medium‑term risks.

A strengthening growth picture

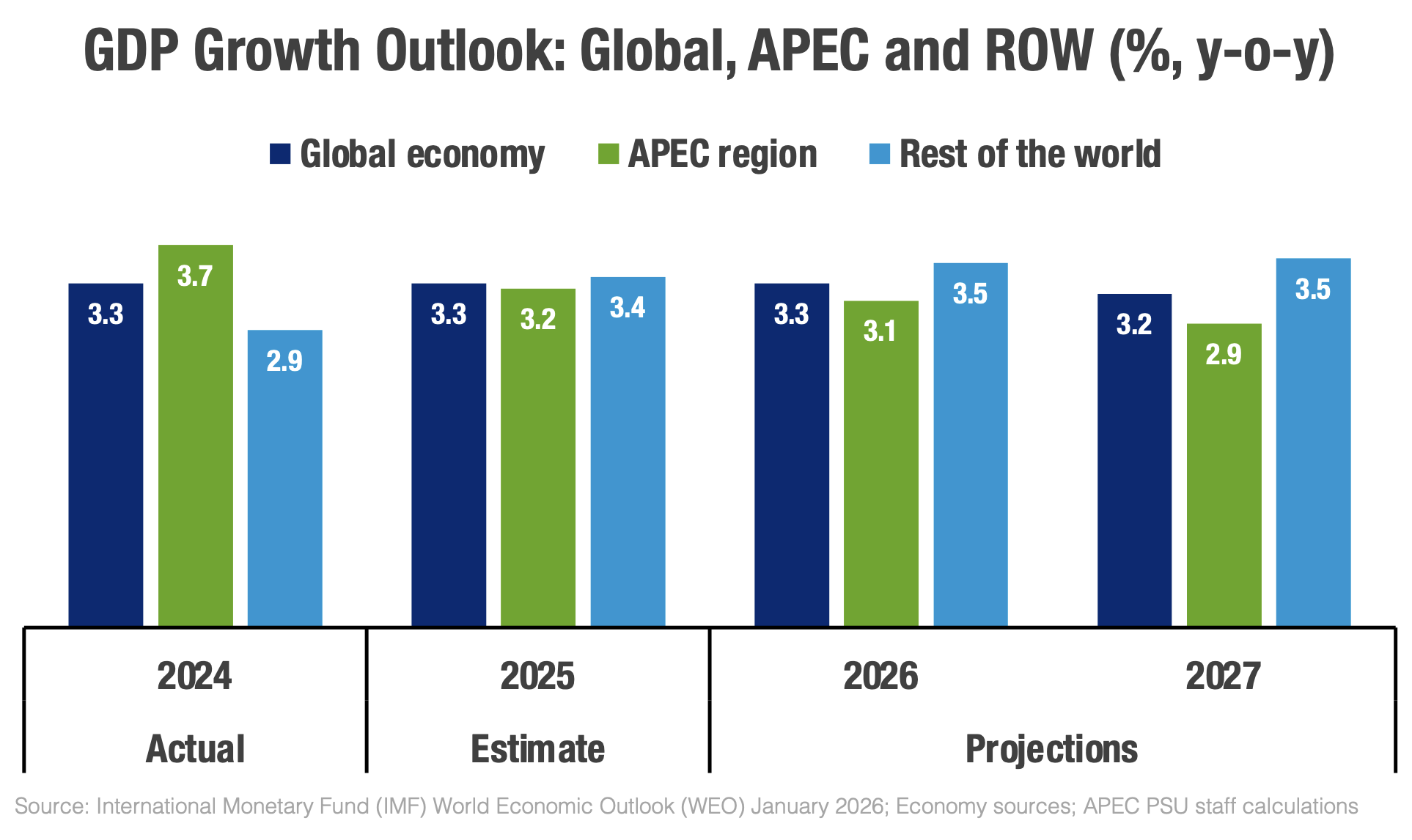

Recent data indicate that the APEC region expanded by 3.4 percent in the first three quarters of 2025, with full-year growth estimated at 3.2 percent, slightly above the October 2025 ARTA projection. This upside reflects stronger-than-anticipated performance in consumption, trade, and investment, particularly in technology-intensive sectors.

APEC growth is projected at about 3.1 percent in 2026, broadly stable and modestly revised upward compared with the earlier forecast of 2.9 percent. This resilience stands out against a backdrop of persistent global uncertainty, highlighting the region's capacity to adapt through flexible supply chains, diversified markets, and continued innovation.

Several factors underpin this improved outlook. Household demand has held up well across much of the region as cost-of-living pressures ease. Trade activity remains robust despite rising protectionism, as firms are rerouting trade flows, adjusting sourcing strategies and diversifying markets. At the same time, massive AI‑related and digital investments are supporting aggregate demand while boosting productivity.

However, large-scale AI investments also raise concerns about concentration and profitability issues, which, combined with prolonged uncertainty and renewed trade protectionism, could heighten medium-term risks and lead to a deceleration in APEC growth, currently projected to slow to 2.9 percent in 2027.

Policy space widens as inflation eases

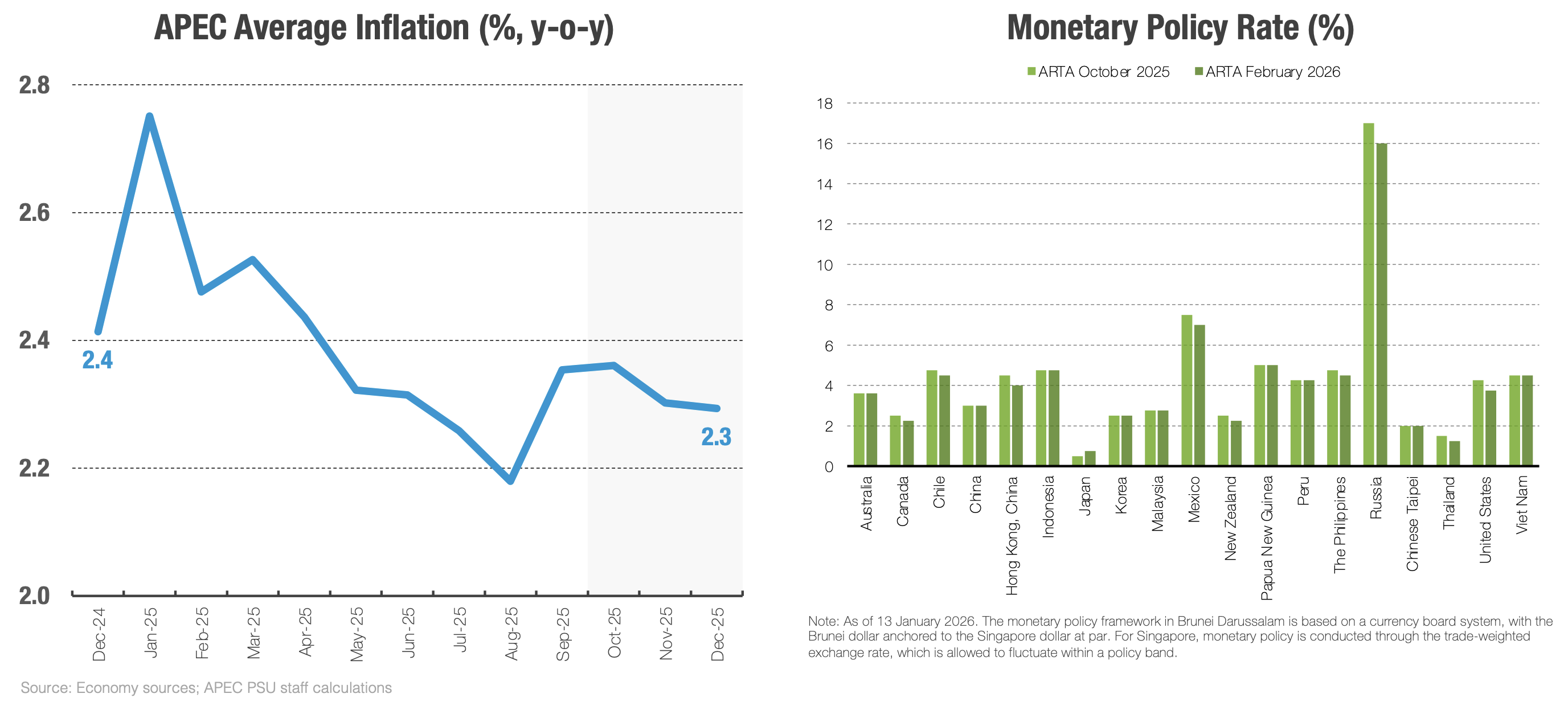

Inflation has continued to ease across most APEC economies. Average inflation in 2025 is estimated at around 2.4 percent, lower than the 2.6 percent recorded in 2024, reflecting softer energy and food prices. Oil prices have declined amid ample supply and rebuilding inventories, while food prices have moderated as agricultural output improved.

This benign inflation environment has allowed many central banks to maintain accommodative or neutral policy stances, supporting domestic demand and investment. Importantly, inflation expectations remain broadly anchored, reinforcing policy credibility. That said, risks to price stability persist, particularly from potential supply shocks, renewed trade restrictions, or geopolitical issues. Preserving strong institutions and prudential oversight remain critical to maintaining confidence as monetary conditions gradually normalize.

Trade resilience amid fragmentation

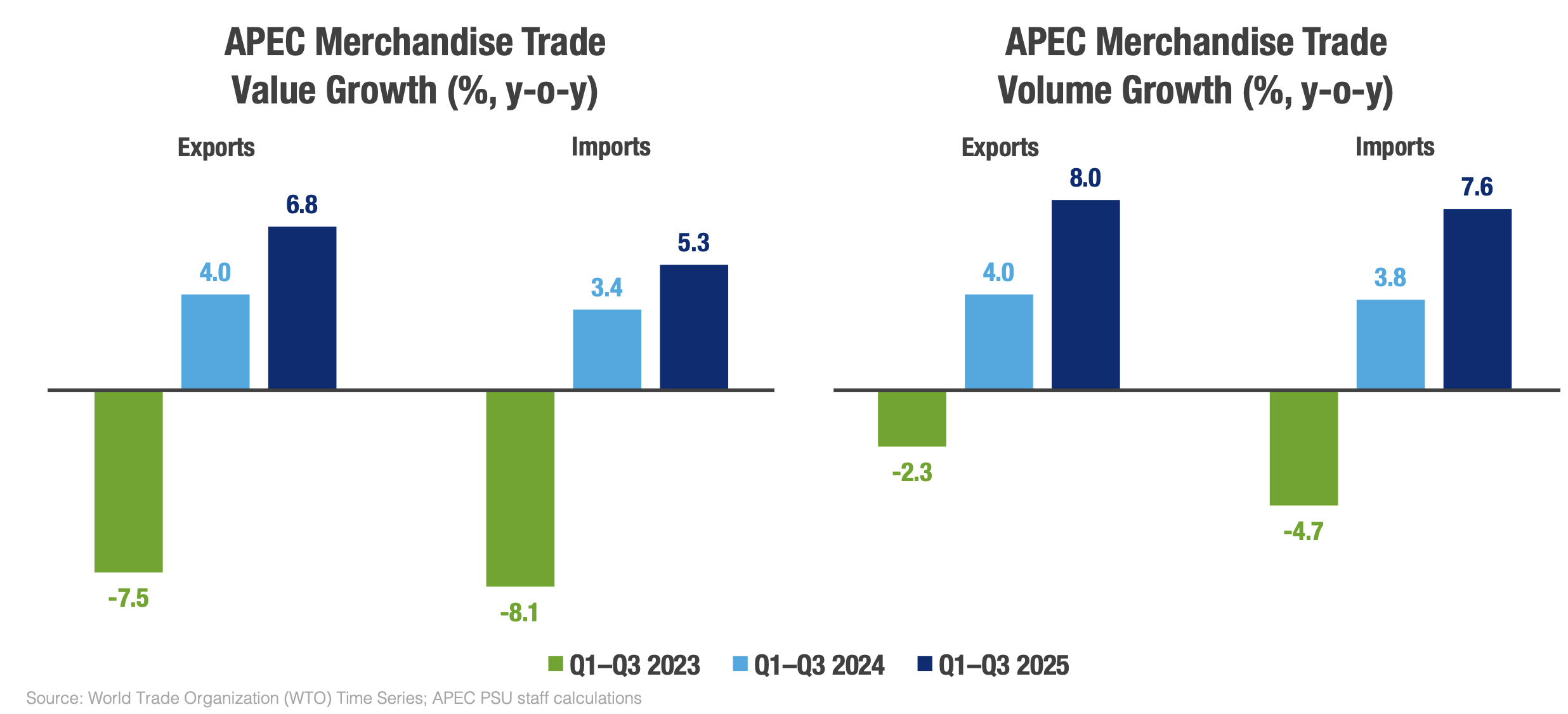

Trade performance exceeds expectations. Merchandise trade volume doubled through the first three quarters of 2025 to 8.0 percent for exports and 7.6 percent for imports compared with 2024, supported by agile business responses to shifting trade routes and sustained demand from technology‑intensive industries.

Intra‑Asia trade has strengthened, reflecting deeper regional integration, while extra‑regional trade has also improved, signaling resilient external demand.

Commercial services trade continues to expand, though at a softer pace than in 2024's rapid rebound. Travel services, in particular, eased from earlier double‑digit growth rates, while transport and other commercial services provided steadier support.

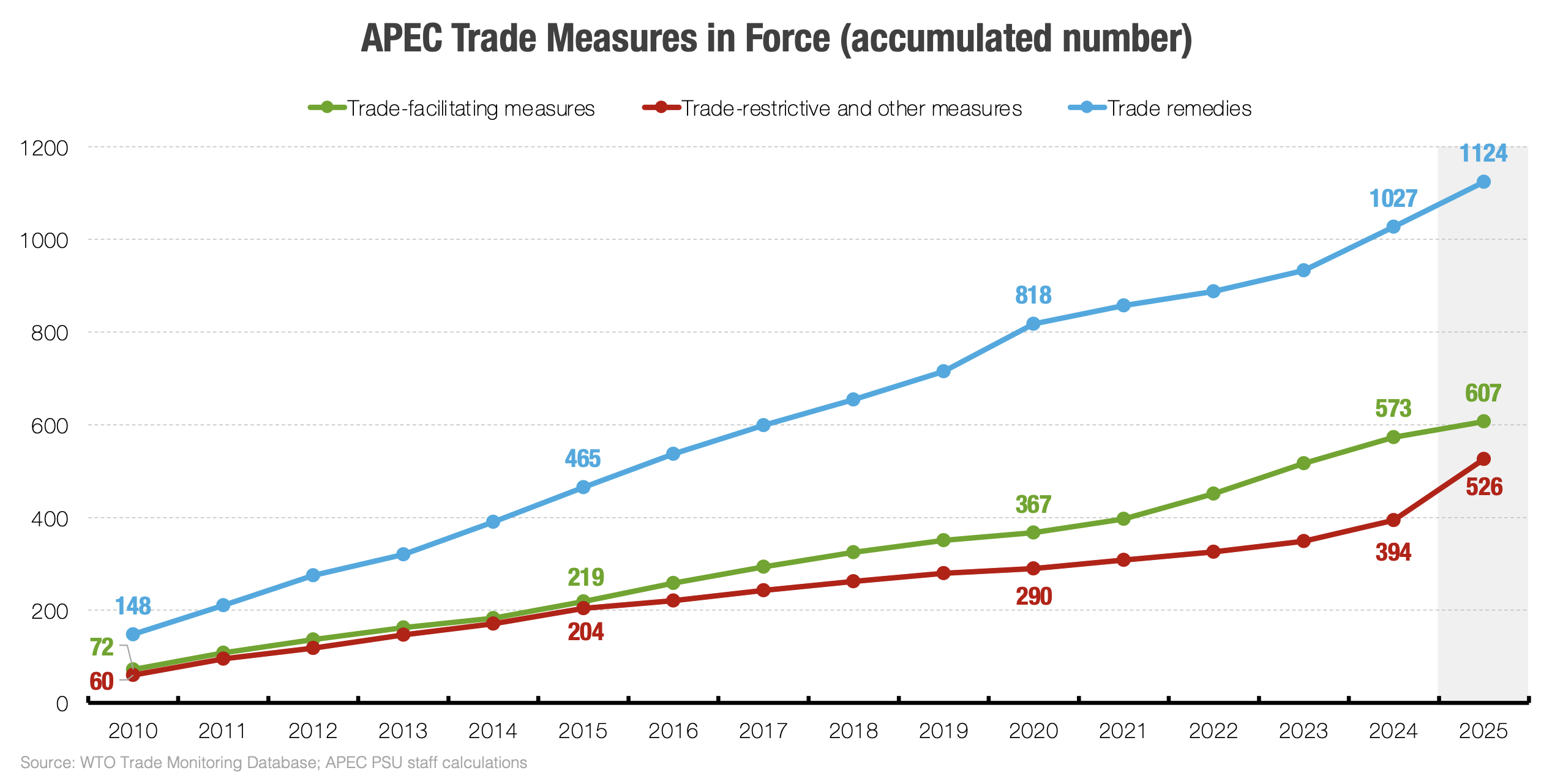

However, these positive trade dynamics coexist with a less favorable policy environment. Trade‑restrictive measures rose sharply in 2025, driven by new tariff and non‑tariff actions. Although economies continue to implement trade‑facilitating measures, these have been outweighed by new restrictions, intensifying medium‑term headwinds. Trade policy uncertainty remains elevated, weighing on business sentiment and investment planning.

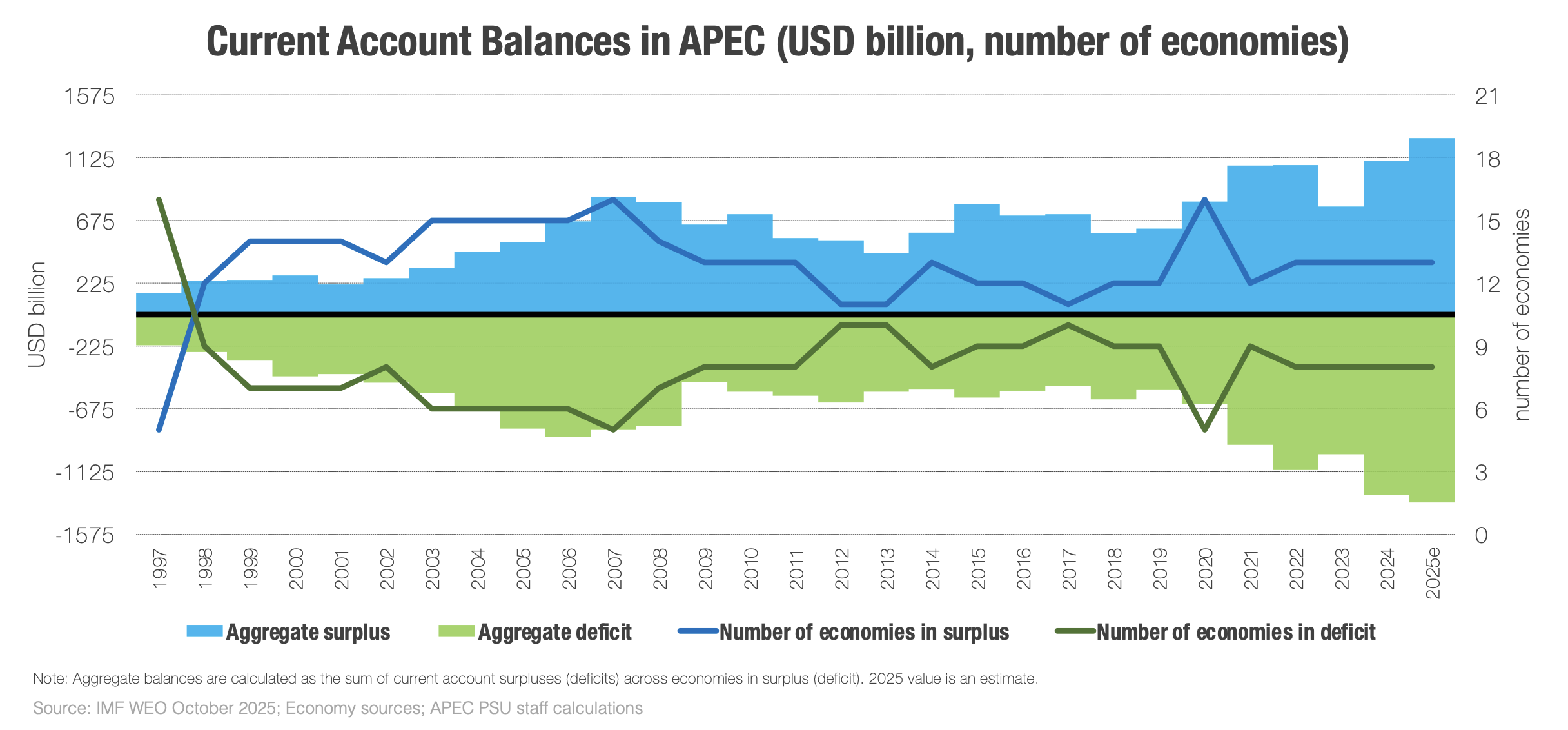

Current account surpluses and deficits have remained persistent across APEC economies and have widened since the early 2020s. These trends reflect structural trade imbalances shaped by differences in savings, investment, competitiveness and domestic demand. While such imbalances can coexist with growth, prolonged surpluses or deficits heighten exposure to external shocks and financial volatility. Strengthening domestic demand and productive investment in surplus economies, while improving competitiveness, export diversification and savings rates in deficit economies, can help sustain growth and reduce imbalance-related risks.

Technology investment: opportunity with risks

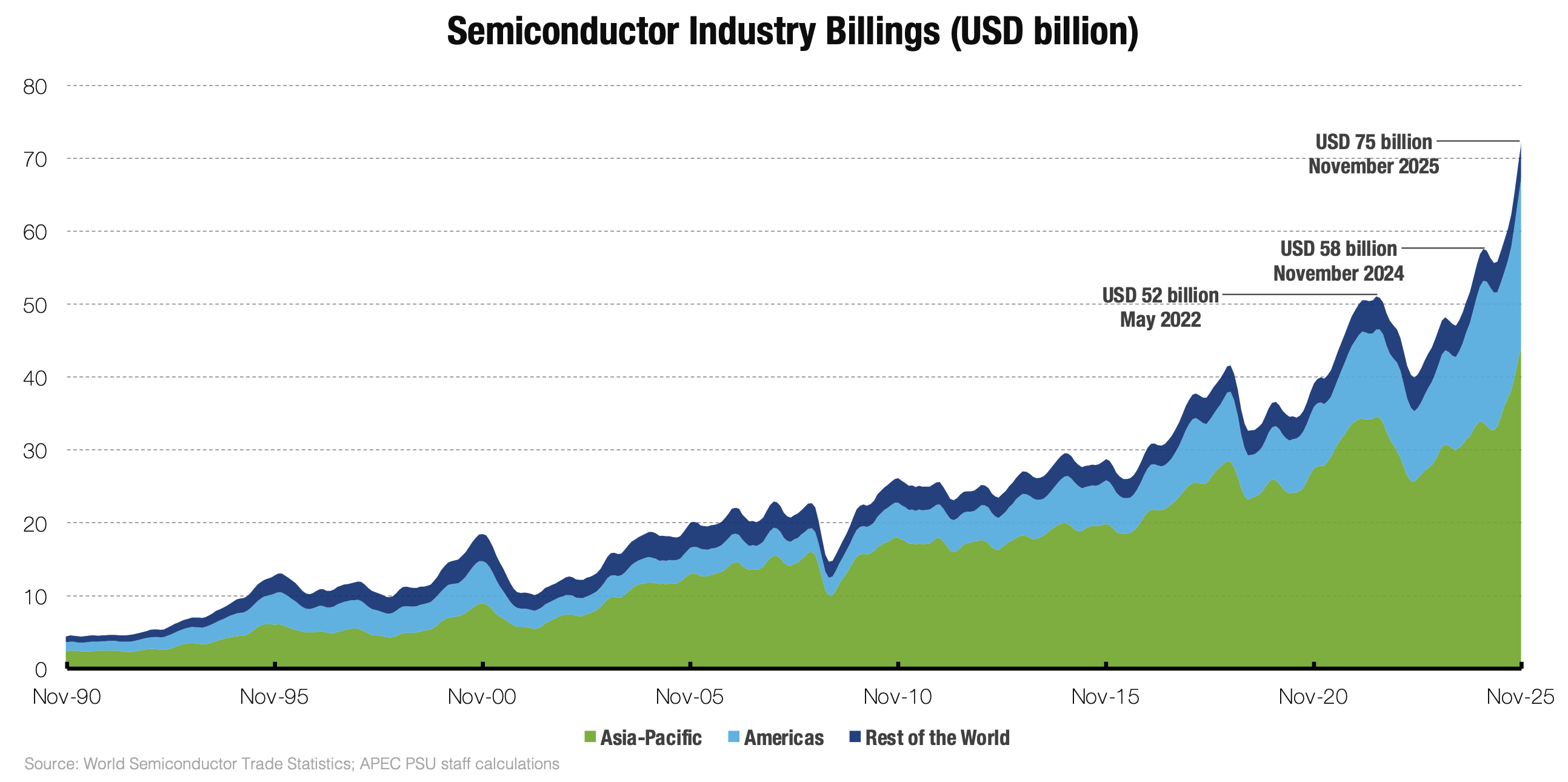

One defining feature of the current cycle is the scale of investment in AI and digital technologies. Global semiconductor billings hit record highs in 2025, driven largely by AI‑related demand. These investments could boost productivity and support longer‑term growth across the region.

At the same time, risks are emerging. Investment has become increasingly concentrated in a narrow set of technologies and sectors, raising exposure to supply‑chain disruptions, geopolitical risks, and the possibility that returns may fall short of expectations. A lopsided investment pattern, over‑reliant on AI as the primary engine of productivity, could increase economic vulnerability if efforts to bridge the digital divide and upgrade digital skills fail to keep pace.

Downside risks and upside opportunities

Despite stronger near‑term momentum, downside risks remain considerable. Geopolitical tensions and geoeconomic fragmentation continue to threaten supply chains and the rules‑based trading system. Prolonged policy uncertainty risks delaying private investment and slowing productivity gains.

Nonetheless, there are notable upside opportunities. The private sector has repeatedly shown adaptability, allowing trade and production networks to reconfigure quickly. Faster‑than‑expected productivity gains from AI, particularly if adoption spread beyond frontier firms, could lift potential growth sooner than assumed. A more synchronized easing of monetary policy, especially among advanced economies, could further support global demand and financial conditions.

Against this backdrop, the ARTA points to three broad policy priorities for APEC economies:

- Reinforcing credible economic management. Easing inflation provides room to support growth, but credibility is critical. Clear policy frameworks and effective prudential oversight help anchor expectations and reduce uncertainty. Strong institutions matter to ensure coherent, credible and market-friendly policies. Effective institutions are key to coordinating policy, managing risks and adapting while preserving trust.

- Promoting inclusive, productivity‑enhancing reform. AI‑driven investment should be paired with broader reforms such as sustained investment in skills development, labor mobility, competitive market structure and reliable infrastructure. Broadening the base of productivity gains that ensures technological progress translates into durable and inclusive growth.

- Strengthening adaptive regional cooperation. In a fragmented global environment, regional platforms matter more than ever. Deeper policy coordination, better information sharing and institutional agility can stabilize expectations and counter rising uncertainty. APEC's role in reinforcing predictability, rebuilding confidence, fostering cooperation and anchoring stability across the region remains vital.

The February 2026 ARTA shows that near‑term growth momentum in APEC has improved, but this is not the time to be complacent. Sustaining current gains will require policies that balance support for demand with reforms that raise productivity and resilience. By leveraging its diversity, adaptability and cooperative frameworks, the APEC region is well-positioned to navigate global transitions, provided that policymakers act decisively to manage risks while seizing emerging opportunities.

Rhea Crisologo Hernando is analyst, Glacer Niño A. Vasquez is researcher, and Carlos Kuriyama is director at the APEC Policy Support Unit.

For more on this topic, download the latest APEC Regional Trends Analysis report.