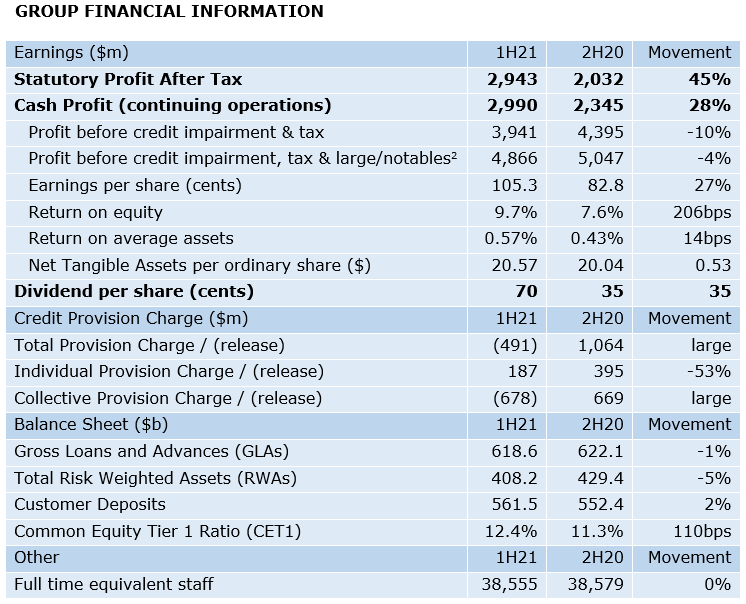

ANZ today announced a Statutory Profit after tax for the Half Year ended 31 March 2021 of $2,943 million, up 45% on the previous half with key drivers including a net credit provision release of $491 million.

Cash Profit[1] for continuing operations, before credit impairments and tax, was $3,941 million, down 10%.

ANZ's Common Equity Tier 1 Ratio strengthened to 12.4% while Cash Return on Equity increased to 9.7%. The proposed Interim Dividend is 70 cents per share, fully franked.

ANZ Chief Executive Officer Shayne Elliott said: "Work done over the past five years to simplify our operations, strengthen our balance sheet and de-risk the Group helped us deliver a strong result this half, meaning we are well-placed to continue to support the ongoing economic recovery and customers doing it tough.

"Following the trends of the first quarter, all parts of our business performed well. Costs were down 2% and we also increased investment in new digital capability that will provide ongoing productivity improvements and better customer outcomes.

"Australia Retail & Commercial had another good half, becoming the third largest home lender in the market. Deposits performed well, with retail and small business customers behaving prudently by building solid savings and offset balances through the half.

"Lower revenues in our Institutional business were largely expected due to the impact of falling interest rates as well as a normalisation of Markets revenue after an exceptionally strong 2020. Our disciplined focus on credit management has been a positive with our largest customers going into the pandemic from a position of strength and adapting fast to the rapidly changing environment.

"New Zealand continued its recent strong performance with record lending growth combined with disciplined cost management. This is a well-run business that is an important part of our overall portfolio and is well-placed to manage increased regulatory capital demands.

"Improving credit conditions resulted in a release of almost $500 million during the half. While the pandemic hasn't resulted in large credit losses to date, we still have almost $4.3 billion in reserve if conditions deteriorate.

"Capital generation was a feature which, along with our already strong balance sheet and prudent management through an incredibly volatile period, meant we were able to return our dividend to a level more in line with our target and sustainable payout ratio.

"Our disciplined approach to capital management also meant we could support customers through the COVID-19 pandemic without the need to dilute existing shareholders through equity raisings."

DIVIDEND & CAPITAL

ANZ's capital position has further strengthened with a Common Equity Tier 1 Ratio of 12.4% (~12.5% on a pro-forma basis[4]), remaining materially above the Australian Prudential Regulation Authority's 'Unquestionably Strong' benchmark.

A combination of strong capital management, solid earnings and improving conditions provided the Board with confidence to pay an interim dividend of 70cps, up from 35cps at the final 2020 result.

ANZ also announced the Dividend Reinvestment Plan (DRP) will continue to apply for the Interim 2021 Dividend at no discount and that it plans to neutralise the impact of the shares allocated under the DRP.

Further, our capital position provides flexibility to return surplus capital to shareholders. Any decision will balance the importance of capital efficiency against maintaining an appropriately strong balance sheet as we continue to get more clarity around the economic situation.

CREDIT QUALITY

The total provision result in the first half was a net release of $491 million which comprises:

- a collective provision (CP) release of $678 million

- an individually assessed provision (IP) charge of $187 million

Despite ongoing uncertainty, the CP release is a result of the improving economic outlook over the course of the half, as well as some loan volume reductions. Home loan and small business customers have also behaved prudently by building savings buffers through the half.

The low IP charge reflects the continued impact of government and bank support packages and our long-term strategy and disciplined focus on customer selection in Institutional. As at 31 March, the CP balance of $4,285 million represents additional reserves of $909 million compared with pre-COVID levels at 30 September 2019.

OPERATIONAL HIGHLIGHTS

Despite a volatile environment with significant demand from customers, we were again able to reduce the cost of running the bank through streamlining and automation, while processing record volumes.

Australia Retail & Commercial

- Provided ~92,000 new home loan accounts, lifting ANZ's position to the third largest home lender in the market.

- Small Business customers who use accounting software platforms can now apply for lending online and get funds within 4 days, reduced from 30 days.

- 42% of all retail sales in Australia, including home loans, are now through digital channels.

- Strong cost outcome with operating expenses down 1% on the previous half and down 2% on the prior comparable period.

New Zealand

- Provided ~42,000 new home loan accounts, maintaining our position as the leading lender in NZ, while also being the first bank to require a 40% deposit from residential property investors in a step to bring balance to the housing market.

- Funds under management for KiwiSaver superannuation at a record level of NZD17.9 billion, up from NZD16.4 billion or 9% during the half.

- Acquired 12 new clearing mandates from customers, taking ANZ's share of NZD wholesale payments to 58%.

Institutional

- Continued focus on winning additional Clearing Services in Australia & New Zealand with market share increasing to 58% (from 51% in November 2020).

- Increased the number of New Payments Platform payments for other banks by 115% when compared with the same period in 2020.

- Introduced the ability for customers to track cross-border payments via our digital platforms, saving around ~35,000 minutes of customer effort in the first week.

Digital & Technology

- ANZ App users increased by 23% when compared with the same period last year and transactions up 26% over the same period.

- Launched the ability for new customers to open an account via the ANZ App; contributing 5% of all new to bank customers across all channels or ~8,000 new customers in Australia.

- Introduced the ability for customers to put a 'gambling block' on credit cards in March 2021 with more than 1,000 customers activating the service in the first month.

CLOSING REMARKS

Mr Elliott said: "While many households and businesses are still doing it tough, Australia and New Zealand are emerging from the sharpest contraction in economic activity in a generation quicker and stronger than many believed possible. This is a credit to Government intervention and the industry working hard to provide customers with the support needed at a critical time.

"There is still significant uncertainty. You only need to look at how the pandemic is playing out overseas, as well as recent lock-downs, to realise how quickly the situation can escalate.

"India, a country in which we have a deep history, is having a particularly difficult time. Despite the circumstances, our team in India are working hard to do their best for our customers and their determination has been inspiring.

"We announced last week a donation of $1 million to World Vision's India's COVID-19 appeal and a further $1 million to match customer and staff donations. We are continuing to do all we can to support our people and their families through this difficult time.

"ANZ is in a strong position both financially and operationally. We are well capitalised and our disciplined approach to costs over many years has us well placed to invest in opportunities to grow our business in targeted segments. The work to digitise core processes and platforms continues at pace and this will be more visible to customers towards the end of the year," Mr Elliott said.

Interviews with relevant executives, including Shayne Elliott, can be found at bluenotes.anz.com.

[1] Cash Profit excludes non-core items included in Statutory Profit with the net after tax adjustment an increase to Statutory Profit of $39m, made up of several items.

[2] Large/notables are items within Cash Profit that, given their nature and significance, are presented separately to provide transparency and aid comparison. Large/notable items were -$817m after tax.

[3] All commentary is presented on a Cash Profit continuing basis excluding large/notable items with growth rates compared with the Half Year ended 30 September 2020 unless otherwise stated.