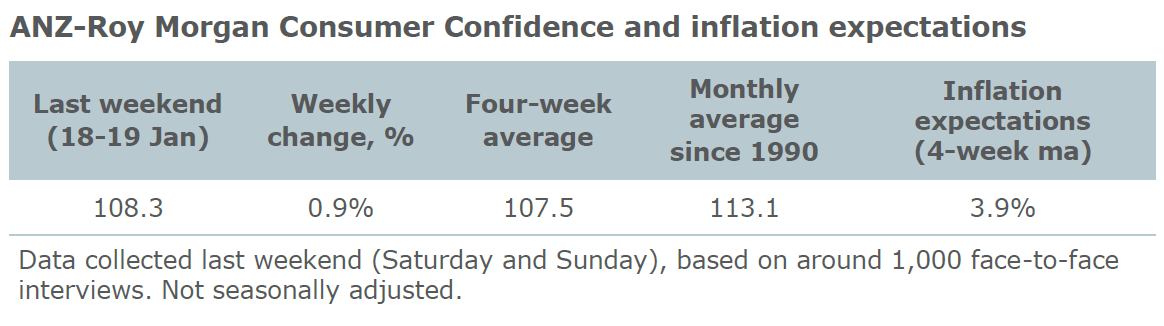

Confidence continued with its forward march last week, gaining 0.9 per cent. This takes it back to where it was in mid-December. The financial and economic sub-indices were mixed, while the 'time to buy a household item' index strengthened solidly.

Current finances gained 3.4 per cent vis-a-vis weakness of 5.5 per cent seen in the previous reading. In contrast, future finances declined 2.5 per cent, reversing some of the 4.6 per cent gain seen over the three previous surveys.

Current economic conditions gained 2.2 per cent, while future economic conditions fell by 3 per cent. These subindices were up 6.1 per cent and 8.6 per cent, respectively, in the previous reading.

'Time to buy a major household item' was up 4.7 per cent, its highest level since October. The four-week moving average of 'inflation expectations' was stable at 3.9 per cent. However, the weekly reading was back above 4 per cent for the first time in two weeks.

"The gain in consumer confidence seen for the second straight week was encouraging, considering the weakness seen in the first reading of the current year," ANZ Head of Australian Economics David Plank said.

"Overall sentiment remains well below average and quite some way below where it was before the Reserve bank of Australia started easing in 2019, however. Some welcome rain during the week may have contributed to the overall rise in sentiment, along with some reasonable local data and the signing of the US-China trade deal Phase One."

"The attainment of a new record for the local share market could also have played a role. The domestic focus this week will be very much on the employment report. A soft result may dampen sentiment somewhat."