If your home was destroyed by a sudden disaster that you couldn't control, you would hope that at the very least, your insurance would cover your losses. However, disaster risk financing systems are struggling to keep pace with growing economic losses. Natural catastrophic (NatCat) events are becoming increasingly costly, and recent global warming could potentially worsen the situation. Researchers at Tohoku University worked together with Swiss RE International SE (Japan Branch) to come up with solutions for more sustainable and cost-effective parametric insurance that supports both victims and disaster risk financing policymakers.

The key problem is that although insured NatCat losses have been rising, the protection gap--the difference between total economic losses and insured losses--continues to widen. This divergence is primarily due to the slow uptake of insurance coverage for NatCat events, which leaves victims without proper compensation.

"Tsunami events are rare, which may be why they are overlooked," explains Anawat Suppasri (Tohoku University). "However, when they occur, they can cause some of the greatest, most devastating losses - even compared to other NatCat events. Despite this, they're often treated as secondary risks in disaster risk financing."

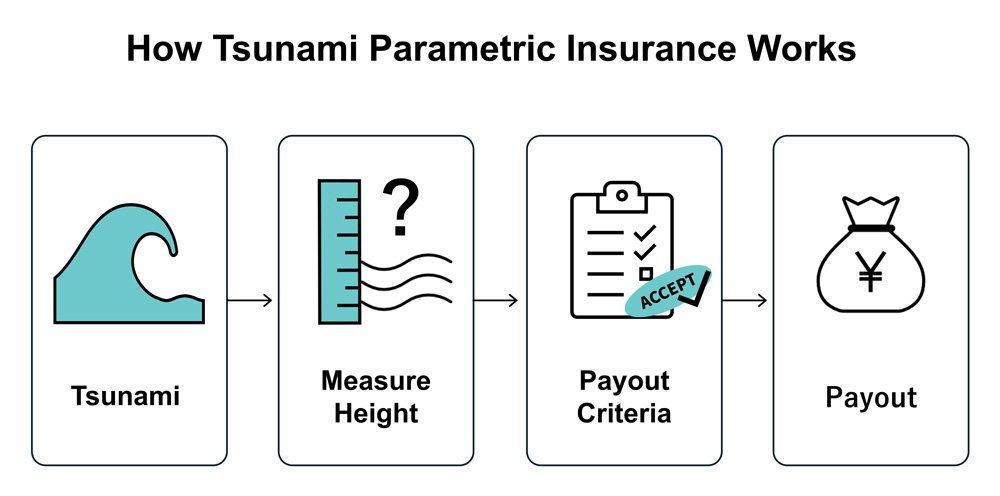

Coming up with an ideal coverage plan is difficult. Typically, a system called parametric insurance is used. The benefits are that it covers losses often excluded from traditional indemnity policies, and that payment is received rapidly, enabling businesses to recover more quickly after disasters. However, the downside is that there is a basis risk: the potential mismatch between actual losses and the insurance payout. They want to compensate disaster victims fairly - not too much (which could drive up premiums and still negatively impact the policyholder), and not too little (falling short of what was destroyed or lost).

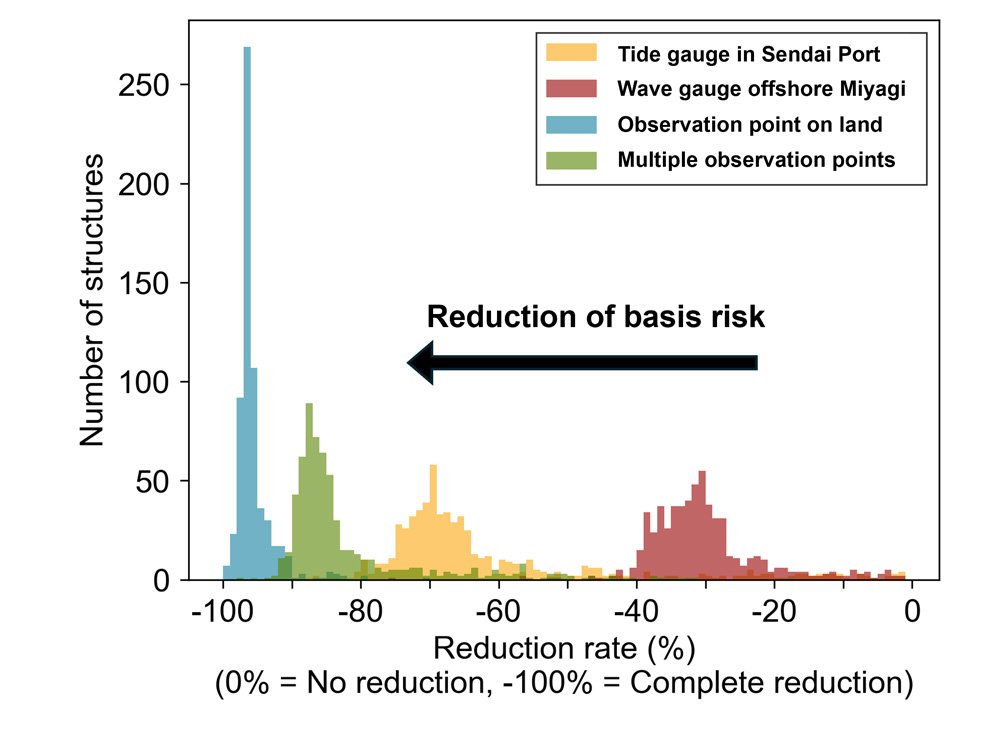

To optimize this balancing act, the research team suggested a customized revamp of a system called parametric insurance. They incorporated Probabilistic Tsunami Risk Assessment (PTRA) into their model to quantify tsunami losses, payouts, and the corresponding basis risk, considering the uncertainty of future tsunami scenarios. In their study, several tsunami indices--such as tsunami height at tide gauges and inundation depth on land--were examined. They identified the optimal payouts and the corresponding thresholds for these indices, which determine when payouts are triggered.

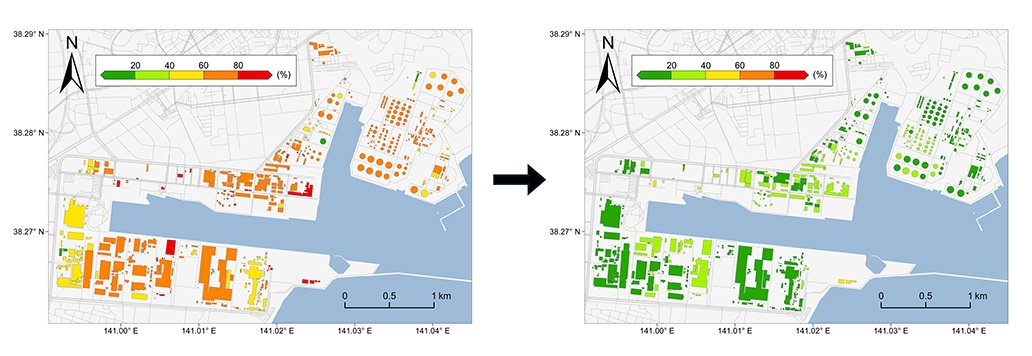

For example, when applied to Sendai Port in Japan, their model reduced overpayment to policyholders by 60.9% while maintaining a reduction in shortfall. This suggests that, for a comparable level of tsunami risk reduction for policyholders, the cost of parametric insurance could be reduced by 60.9%. This means that victims get paid fairly more often and companies can operate efficiently without overpayment errors.

The proposed framework may aid financial institutions in developing more robust parametric insurance products for tsunami events and support their expansion into other tsunami-prone regions. Given the destructive aftermath of tsunami events, an efficient insurance plan may not just mean saving money - but also saving lives.

The findings were published in npj Natural Hazards on July 21, 2025.

- Publication Details:

Title: A proposed approach towards minimizing basis risk in tsunami parametric insurance scheme

Authors: Yushi Miki, Constance Ting Chua, Anawat Suppasri, An-Chi Cheng, Tomoya Iwasaki, Yugo Shinozuka, Takafumi Ogawa and Fumihiko Imamura

Journal: npj Natural Hazards