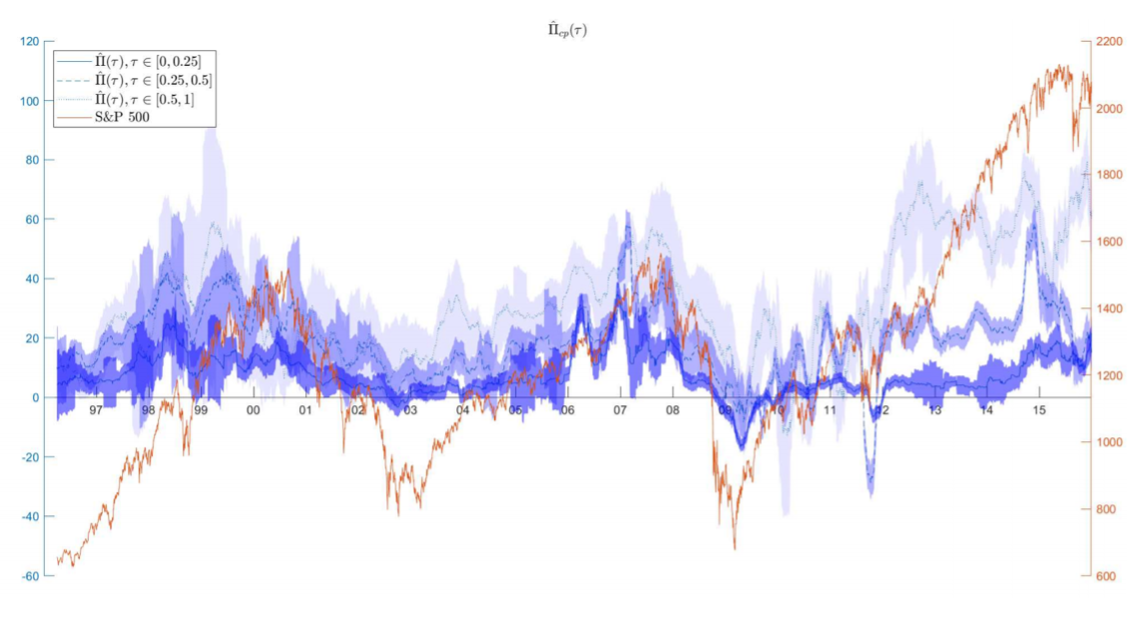

S&P 500 index (in red) and its bubble interval estimates (in blue, for various liquidation dates) over 1996-2015. Bubbles were positive and economically significant in the late 1990's, during 2006-2007 (prior to the GFC), and after mid-2014.

Did you hear the one about the rural New Jersey deli worth $146 million? Financial bubbles are getting so big they're almost becoming punchlines. But what if you could find them before they burst?

New research by the University of Sydney and Cornell University offers a new method of identifying bubbles in real-time using cross-sectional option price data, with implications for reserve banks and traders alike.

"Policy makers like those in reserve banks can use this methodology to make macroeconomic shifts or issue warnings, to prevent bubbles that could negatively affect the general public," said co-author, Dr Simon Kwok from the School of Economics.

"On the other hand, traders can use our method to 'ride on a bubble' for maximum profit. Over the period we sampled, the trading strategy derived from our S&P 500 index bubble estimate earned a net profit of 8.7 percent per annum, compared to the buy-and-hold strategy which earned 5.1 percent per annum."

First, get the sale prices of the stock option contracts at various strike prices. They are useful for uncovering the distribution of discounted future stock prices. Then calculate the fundamental stock value as the average of discounted future stock prices. Subtract this from the observed spot (current) stock prices to obtain bubble estimates

The method diverges from traditional ways of predicting bubbles that entail sensitivity to model choices and require time series data of asset prices. Instead, it relies on cross-sectional option price data.

"It's simple," Dr Kwok said. "First, get the sale prices of the stock option contracts at various strike prices. They are useful for uncovering the distribution of discounted future stock prices. Then calculate the fundamental stock value as the average of discounted future stock prices. Subtract this from the observed spot (current) stock prices to obtain bubble estimates."

Together with Professor Robert Jarrow from Cornell University, he examined daily prices of European call and put options written on the S&P 500 index spanning 1996 to 2015 and found strong evidence of the existence of bubbles. Their sizes were economically significant, taking up more than three percent of the index during 2006-2007, just before the start of the 2008 Global Financial Crisis.

"Big financial bubbles are a cause of concern because they are unsustainable and, once they burst, can lead to catastrophic loss of wealth. This is evident from the 2000 dot-com bubble and 2007 housing bubble," Dr Kwok said.

The method is applicable to any market indices or stocks that have liquidly traded options. The ASX 100 index and blue-chip stocks such as those of the big four banks fall into this category.

A pre-print of the paper is available online and is forthcoming in print in the Journal of Applied Econometrics.

Declaration: Dr Kwok received funding from the School of Economics to present the paper at two online conferences, IAAE 2021 and NASMES 2021.