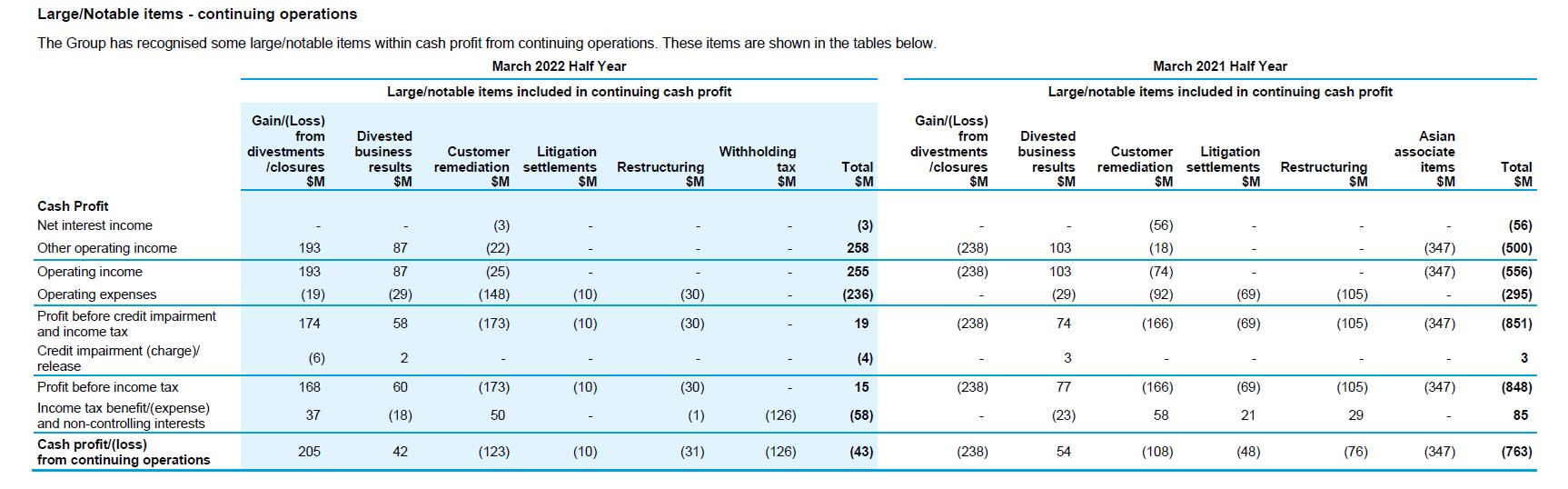

ANZ today announced its first half 2022 Statutory and Cash Profit will be impacted by a number of large/notable items with a net after tax charge of $43 million (minimal impact on CET1 capital):

- Net after tax gain of $205 million relating to divestments and business closures during the period primarily driven by the gain on sale of the Merchant Acquiring Business in exchange for a 49% interest in a new ANZ Worldline Payment Solutions partnership[1].

- Tax charge of $126 million relating to withholding tax on a dividend payment from ANZ Papua New Guinea. A capital injection was made into ANZ Papua New Guinea equivalent to the dividend, net of withholding tax. This was to rebalance capital positions within the Group in response to APRA's changes in the capital requirements for subsidiaries[2].

- After tax charge of $123 million in respect of customer remediation, covering increased program costs and revised estimates to customer remediation predominantly in the Australia Retail and Commercial division.

- Net after tax gain of $1 million comprised of restructuring charges, divested business results and a litigation settlement.

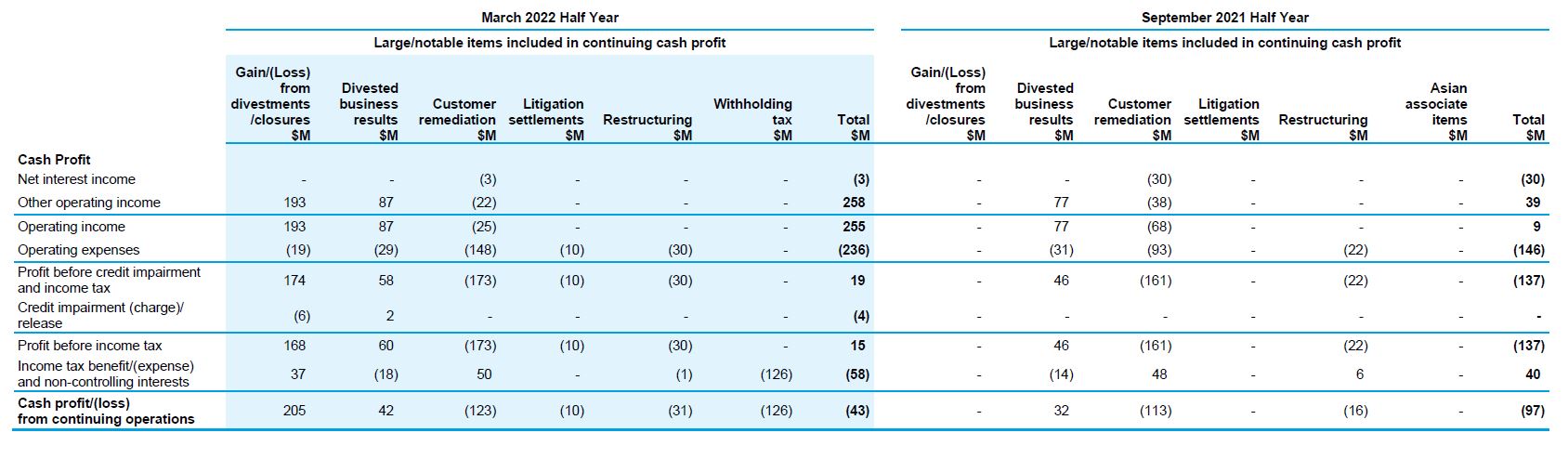

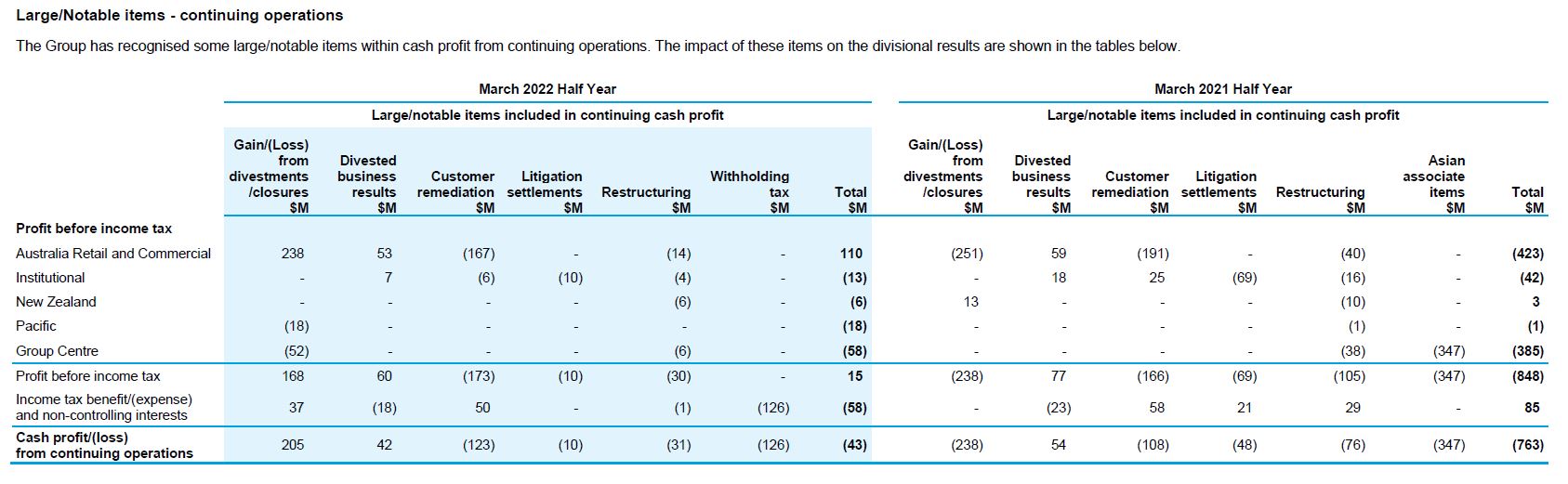

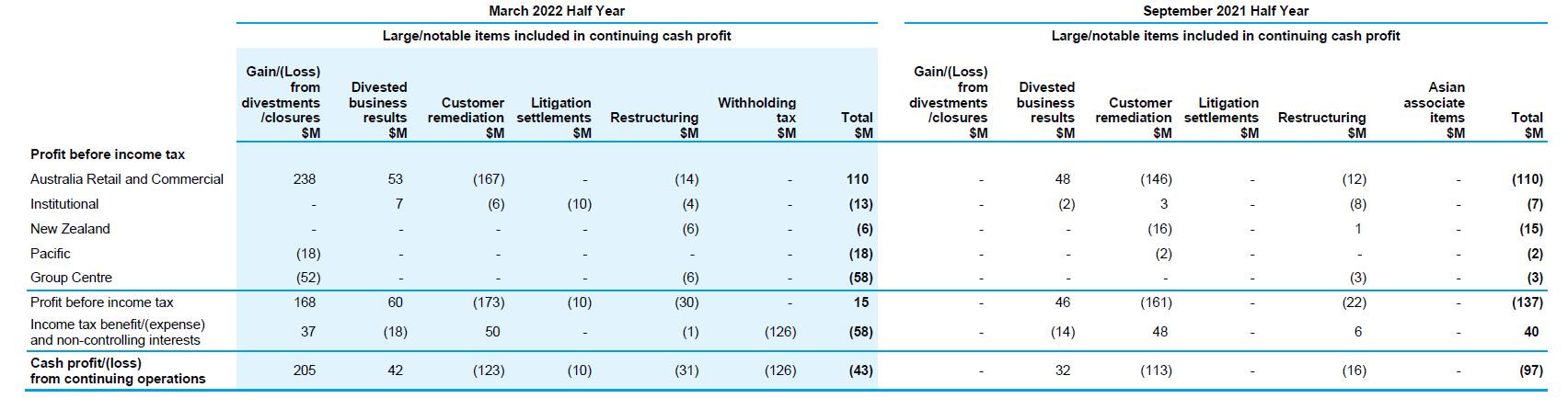

The relevant large/notable items (continuing operations) templates, reflecting the tables that will be shown in ANZ's First Half 2022 Consolidated Financial Report & Dividend Announcement, are included on the following pages.

ANZ's First Half 2022 result will be announced on Wednesday 4 May 2022.

[1] See ANZ announcements of 15 December 2020 "ANZ enters joint venture with Worldline" and of 1 April 2022 "ANZ commences joint venture with Worldline".

[2] See ANZ announcement of 15 October 2019 "APRA - subsidiary capital investment treatment update"

/Public Release. This material from the originating organization/author(s) might be of the point-in-time nature, and edited for clarity, style and length. Mirage.News does not take institutional positions or sides, and all views, positions, and conclusions expressed herein are solely those of the author(s).View in full here.