Key points:

- The United States Department of Agriculture (USDA) has revised American beef production forecasts up for 2023

- Increased US production has increased available supply on global markets

- The outlook remains strong for Australian beef exports, especially in 2024.

Last week, the United States Department of Agriculture (USDA) released the July Livestock and Poultry: World Markets and Trade report, which includes beef, pork and poultry forecasting in several key markets.

For Australian producers, the most important shift was an upwards revision of the US beef production forecast, which rose 1.4% to 12.4 million tonnes compared to the April report. This is still well below the 12.9 million tonnes produced in 2022, but the revision reflects slower-than-expected American pasture improvement and high US cattle prices encouraging turn-off.

Export patterns shift

The relative strength of American beef production has implications for Australian exports, both over the past few months and in the future. Australian beef exports in the first half of the year were up 20% on the first half of 2023; however, exports to Japan (the largest market for Australian beef) have been down 6%.

Japan normally sources over 80% of its imported beef from either Australia or the United States, and the two exporters both compete and complement each other in market – the Australian cattle cycle usually peaks as the US falls and vice-versa, creating relative consistency of supply in the market.

So far, the continued strength of American production has pushed US exports higher than expected, which has temporarily suppressed demand for Australian beef. In the year-to-May 2023, 43% of Japanese imports came from the US, compared to 37% for Australia.

This has meant that Australian product has largely gone to China, where demand has been slowly but consistently strengthening, and the US, where Australian beef is a crucial input in mince and burger production.

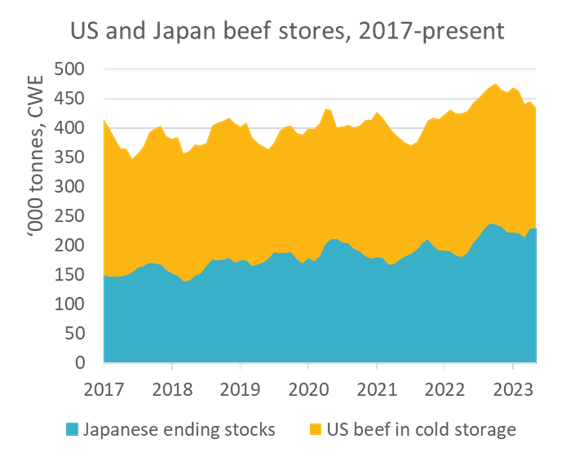

Cold stocks remain high

Additionally, beef stores in both Japan and the US remain relatively full compared to historic norms. Although US cold stores have come down since a peak in September 2022, they remain elevated, and Japanese accumulated stores have remained at all-time highs. Even as production comes down in the US, there is a substantial 'stockpile' on both sides of the Pacific that will essentially buffer any changes to demand. Importers will be able to draw down supplies of frozen beef for a period to make up shortfalls.

Figure 1: US and Japan beef stores from 2017 to present

Source: ALIC, USDA, MLA calculations

Looking forward

Although the increase in US supply has had a temporary effect on Australian export prices, it is ultimately a positive for Australian exporters in the medium term.

The US cattle herd has been shrinking since 2019, and female slaughter remains well above historic norms in 2023, even as overall slaughter has declined. This means that the American breeding herd is still shrinking, which will impact the speed and intensity of the US herd rebuild. Already, American cattle prices have reached new peaks as demand remains consistent compared to a rapidly shrinking supply.

Although substantial reserves of frozen beef will slow the rate of change in demand for Australian beef, continued drawdowns of beef and a shrinking US herd mean that supply will come down over time, and Australian exporters will be well positioned to meet the resulting demand.