Introduction

I'm honoured to contribute to this storied lecture series. I'm a past attendee of many 'Beesleys', and one of the nice traditions of the Beesley lectures has been that those who knew and worked with Michael Beesley take a moment to recall him before diving into their lectures. I've listened to those accounts over the years. As well as his warmth and collegiality and his loyalty to Birmingham, what shines through was his appetite for debate, fascination with markets and conviction that good economics had a lot to offer policymaking. That this lecture series is going strong into its fourth decade seems a fitting legacy.

My topic tonight is EV charging infrastructure, and the UK's efforts to secure the investment needed to electrify road transport. It is a case study illustrating how markets can contribute not only to economic growth but to a societal goal like de-carbonisation. All the major themes of competition and consumer policy in 2022 arise: the need for markets to operate alongside government policy; the economics of a consumer necessity, the car, in a cost-of-living crisis; the backdrop of rising energy prices; how to foster innovation; how to deploy infrastructure widely, minimising the risk of enclaves or deserts, whilst preserving competition.

I am speaking this evening in a personal capacity. The views are mine and not necessarily those of the CMA or my colleagues (Endnote 1). That said, I want to acknowledge that almost all the work I'll discuss was done by others - especially my colleagues in the CMA's Markets team, led by Daniel Gordon, and the EV charging market study team, directed by Emily Chissell and Sabrina Basran, supported by the CMA's economists, lawyers and financial analysts. I'm also grateful to many colleagues and practitioners inside and outside the CMA who offered comments or insights as I prepared - a full list is in the published version. (Endnote 2)

My focus is the system in which competition authorities and regulators act to make markets work better. How well do we identify market failures? Are we designing practical and effective solutions to mitigate those problems? How do we make space for other objectives, that aren't about markets or competition specifically, in a principled and predictable way?

With that in mind, my plan for the next 45 minutes or so is:

First, to briefly survey the problem: why we are going to need a lot more EV charging infrastructure to meet the Government's Net Zero ambition.

Second, to consider the policy framework supporting investment in public charging infrastructure.

Third, to consider the lessons to be drawn from other sectors or parts of the competition and consumer policy toolkit that might be helpful.

The nature of the problem

EVs are not new but petrol vehicles have long-standing benefits

Electric vehicles are not new. The first electric vehicle was launched in 1884, but petrol vehicles rapidly displaced them.

The advantage of electric over petrol has always been that EVs are quiet and efficient, without emissions at the tailpipe.

The disadvantage of EVs is energy storage: fuel tanks contain far more energy in a much smaller space than any battery yet invented, and pumping petrol is faster than charging a battery. So petrol vehicles have greater range, and refill much more quickly, than EVs.

EVs in climate change policy

The case for EVs - or more accurately, the case against petrol - is grounded in our need to de-carbonise our economy. (Endnote 3)

Everyone here knows the backdrop of the UK's 2050 net zero commitment. Today, transport constitutes around a quarter (23%) of UK's CO2 emissions - the biggest single source - almost all of it from road transport, mostly cars (Endnote 4). Coupled with a move to low carbon or carbon free generation, electrification is on the critical path to Net Zero.

To achieve this, the UK is phasing out new petrol vehicle sales from 2030, with hybrids not sold after 2035. Emissions from cars, commercial vehicles and trains are targeted to reduce to a quarter of 2019 levels by 2035 - just under a quarter of the UK's de-carbonisation commitment. Rapid take-up of electric vehicles isn't the only element; petrol vehicles will use more biofuels and the Government aims to scrap older, dirtier vehicles more quickly (Endnote 5). There's also work underway getting people to walk, cycle and scoot more, and drive less.

But EVs are set to take centre stage.

Types of EV charging

The time to charge an EV depends on power output. Overnight charging at home only needs a trickle of power, drawn from the existing grid at off-peak times; charging en route on a long journey in less than half an hour takes very significant power, specialised equipment and often major upgrades to the electricity network.

We can distinguish between private charging (in a driveway or garage, or the workplace), and public charging, where charging is offered to the public.

Home-charging is generally a one-off purchase and installation. It relies on the users' home energy contract. This works well: most EV buyers with space to do so buy a home charging point. A government scheme (Endnote 6) has helped promote this (Endnote 7). Workplace chargepoints are also growing quickly (Endnote 8).

Public EV charging raises a 'chicken and egg' problem: buying an EV is only attractive if you expect public charging to be available where and when you need it. And building EV infrastructure only makes sense if there are lots of EVs on the road to be your customers.

This is not an unusual problem - it often arises in technology markets (getting two groups of users interested in a new digital platform), or in industries like payments, in the business of bringing together buyers and sellers.

In practice, the challenge in EVs is even more complex, since consumers need a mix of charging options - if you buy an EV, you will regret it if you can't charge at home, or locally, or at work, or you can't undertake the longest journey your family plans that year. Consumers are acutely aware of this constraint. That's why the National Infrastructure Commission, for example, concluded this year that 'the big barrier for expanding EVs ownership and the transition to a net zero transport sector remains the rollout of charging infrastructure' (Endnote 9).

A critical element in solving this problem for EVs was the government's decision to set a date for the end of sales of petrol vehicles in 2030. That has had a big impact: awareness of EVs is high and more consumers expect to go electric for their next car than petrol (Endnote 10). Given that impact - and recognising that it carries some risk - it is worth noting that this intervention has very little direct cost. It shapes the market trajectory, effectively firing the starting gun in a race to deploy charging infrastructure in a way that will support that switchover.

Business/operating models

With charging largely outside the scope of retail energy regulation, various business models have been adopted in response (Endnote 11). One EV manufacturer, Tesla, offers its own network for charging almost exclusively for Tesla EVs; other networks can generally be used by any EV. Amongst chargepoint operators, in some cases a full operator funds the infrastructure and sells charging directly to the public; a service provider might provide a chargepoint to a site for a fee, with the site owner then deciding how to offer charging (which might be free, to encourage visits or as a benefit to employees). Some sites operate as concessions - like a full operator but funded through grants - widely used by LAs to achieve rapid roll-out of new sites. Chargepoint operators are typically owned by car manufacturers (Endnote 12), investment funds (Endnote 13), forecourt operators (Endnote 14), or major oil companies (Endnote 15). We have seen new entry and innovation across the value chain.

There is great uncertainty associated with many of these business models. 'Petrol-like' consumer expectations - drive up, charge, drive away - are the hardest and most expensive to fulfil. For en-route charging, that model seems inescapable, but for most driving, given time, and provided there are price signals, new consumer behaviours may develop as EVs become prevalent.

Predicted utilisation is sometimes low, especially in areas where the density of EVs remains low. Some operators are betting on forecast increases in usage as EVs become the norm. Some low utilisation installations may help adoption even if they aren't used very much - people want to know that there is a wide network of chargers before they buy an EV, even if they only ever drive locally. Building these may only occur if they are subsidised.

Scale of the challenge

So how are we doing? The Climate Change Committee tracks overall progress towards net zero targets and sets benchmarks for progress on a range of metrics.

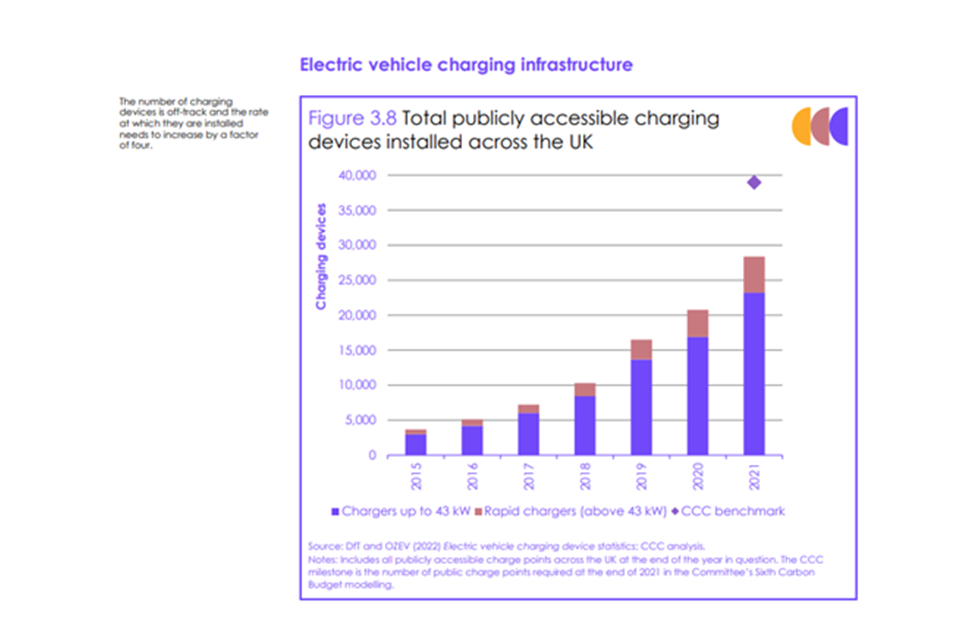

Their view was that the UK needed 12 times more public charge points than it had in 2021 to be ready for 2030 - 27k new charge points per year - with especially strong growth needed in mid to high power range charge points, for example 50kW plus (where the number of chargepoints forecast to be needed was more than 40x the number then installed).

In their 2022 assessment, the Committee's conclusion is that 'the number of charging devices is off-track and the rate at which they are installed needs to increase by a factor of four' (Endnote 16). Here is the shortfall today:

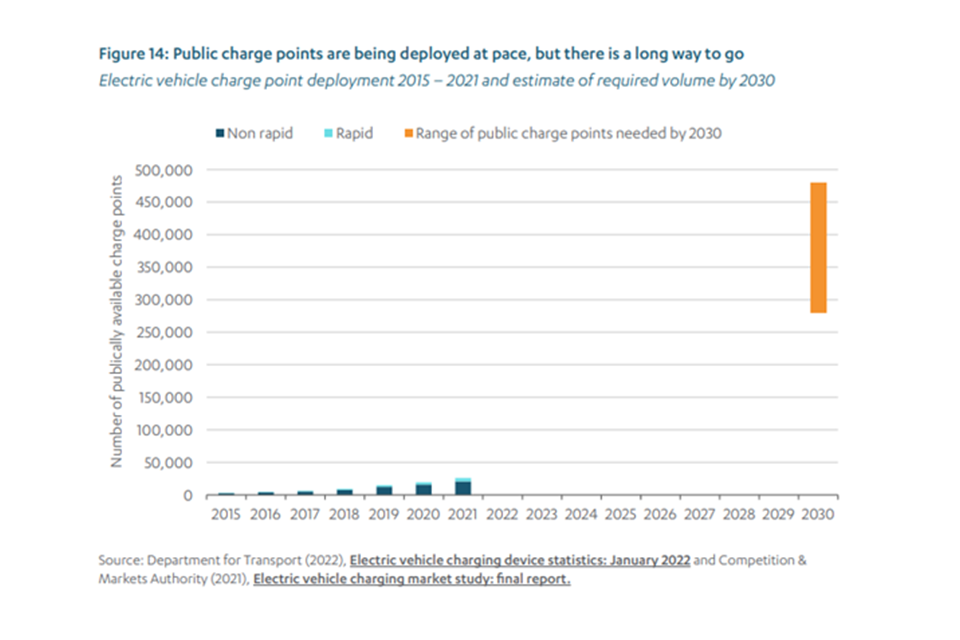

And here, more starkly, is the NIC's view on the overall trajectory, using the same data (Endnote 17).

The investment challenge

To build infrastructure on this scale demands significant investment - probably at least five to ten billion pounds for the chargepoint networks (Endnote 18), and a material amount in the electricity network. We already see significant private investment, and competition between chargepoint operators. But levels of investment will need to increase markedly as EVs grow.

If chargepoints don't grow in line with EVs on the road, then drivers may face capacity issues - that is, queues or delays (Endnote 19). As well as capacity, there is also coverage to consider: there is a risk of duplication in some areas, and lack of service in others - as has occurred with ATM deployment, for example.

To attract investment, public chargepoints need to be profitable - they will only recoup investment when they are used at a price that covers their costs. For public charging, this is risky early on, when EVs are less well-established and consumer charging practices are still developing. Demand uncertainty affects the type of private sector investment attracted to the sector (deterring investors seeking long-term low risk infrastructure investments).

Early private investment in charging was focused where demand, and hence returns, are strongest - home and workplace charging. Investment has been weaker on en route and on-street charging, where business models are more complex and risky. Worst of all is public charging in remote areas, where some deployments may never be profitable without subsidy. But these are precisely the types of charging that reduce consumer barriers to take-up.

Impacts of EVs on the electricity network

Increased demand

EVs increase demand for electricity, and require greater capacity, often in new or unusual places (for example, alongside motorways). Demand is expected to increase by around 20-30%, with transport accounting for around a fifth of all electricity demand (up from virtually none today) (Endnote 20).

Electricity network operators are therefore critical players in EV adoption. If public charging is the norm, local networks (DNOs) need to upgrade connections and strengthen the network. National Grid needs to ensure that the transmission infrastructure can meet these new demands.

Connectivity

When charging was first launched, the cost of upgrading the electricity network was carried in the business cases for new chargepoints. That lead to high incremental costs and in some cases, very lumpy outcomes, as capacity is exhausted. Ofgem has since taken steps to spread these costs over a wider set of customers.

Separate from costs, delays in securing network connections have also been a concern. Operators have argued that a more transparent and timely process would significantly help the faster roll-out of chargepoints at scale. This is linked to wider problems with network pricing, including the lack of locational pricing - although that might help in some ways and make other concerns, such as access in remote areas, even harder.

Smart charging

On the other hand, EVs also provide a new way to make the electricity grid more efficient.

Smart charging - that is, the use of home and work charging points that are linked and able to be coordinated - enables better use of network assets by shifting demand away from peak periods, and by charging when the wind is blowing, and the sun is shining. Electricity can also flow out, with EVs exporting stored electricity during periods of high demand or low electricity supply.

Early trials seem quite positive, and Ofgem has made this a priority, recognising the potential to achieve substantial shifts in peak EV demand. These benefits are a potential externality arising from EV adoption - only some of these benefits can easily be captured through market signals (such as time of use tariffs) in slower EV charging which provides them. More generally, they are also likely to work best only if there is a successful shift to a smart energy network more generally, with half-hourly charging providing incentives on network operators and energy suppliers to offer tariffs to consumers that reward shifts in consumption away from peak times.

Taking stock

So, to recap: early take-up of EVs and deployment of charging infrastructure has proceeded rapidly. Consumers are largely on board. We are starting to see the sort of growth associated with other mass-market adoptions of consumer technology.

But the glass is half-empty: the UK is off-track in terms of meeting the Net Zero target. To achieve it, the UK needs to quadruple the pace at which new public chargepoints are installed. For that, major new investment will be needed in chargepoints, as well as a significant upgrade to the electricity network.

Policy framework supporting EV charging infrastructure

This need for investment creates a public policy challenge. The environment facing investors is complex, encompassing many different public bodies. First, central Government (for fiscal support and the net zero target itself). Next, the devolved administrations, especially in relation to devolved powers such as transport policy and planning. Finally, local authorities for local planning decisions and permits for streetworks, as well as each being a major site provider. And there are a slew of statutory agencies to consider, including Ofgem and URGENI, OZEV and so on.

UK government strategy

It is therefore welcome that in March this year, the UK government published Taking charge: the electric vehicle infrastructure strategy that aims to ensure that charging infrastructure is not a barrier to the adoption of electric vehicles (Endnote 21). Having a clear and ambitious national strategy set by central Government was the first recommendation of the CMA's market study.

The strategy recognises that today's roll-out is too slow. Public charging has not always been as reliable or fast as consumers have a right to expect. The business case for deployment of new chargepoints is hard in areas of low utilisation or where connection costs are high. Getting those connections from the energy network operators can be slow and expensive. And finally, that there is a need for local engagement, leadership and planning.

In response, the government focuses on two interventions: one, to accelerate the roll-out of high-powered chargers on the strategic road network through the Government's £950m Rapid Charging Fund, and second, to transform on-street charging by setting an obligation on local authorities to develop and implement local charging strategies in their areas.

Equally importantly, the strategy winds down existing subsidies that are no longer needed, for example, for home chargepoints.

Finally, the strategy rightly focuses on the consumer experience. It sets a clear direction in favour of open data, price transparency, widely-accepted payment methods and reliability.

There are risks to consumers from government direction-setting. These can be partly mitigated by leaving space for experimentation and differentiation about how to execute the strategy. But clearly, if we have an important national priority to decarbonise transport, then it is a good idea for both private and public actors if there is a clear strategy about how to do so.

To execute this strategy there is a complex set of interventions which I'm not even going to attempt to survey exhaustively. But in keeping with my focus on our competition and consumer framework, I want to draw out a few points.

EV policy builds on established principles

First, the approach to EV charging reflects our competition and consumer policy framework generally. The approach varies by the scope for competition:

-

Charging infrastructure is generally competitive. Markets will drive investment. The CMA can help promote competition using the tools that promote and protect competition across the whole economy. Specific rules will be set to deal with specific problems.

-

The electricity network supporting charging is a monopoly. Investment will be broadly governed by regulation. Ofgem sets rules designed to mimic the constraint that competition would otherwise provide.

Separating out and regulating monopoly elements to enable competition elsewhere is a foundational element of UK competition policy, visible in virtually every sector-specific regime, from major airports, telecoms, or as in this case, energy networks.

This approach ensures that the monopoly energy network cannot foreclose competition in chargepoints. But it creates a new challenge: to coordinate investment between them.

Policy can vary in different parts of the UK

Second, the approach supports variation between different nations of the UK.

In England, the model is primarily private sector investment in public charging (with a more mixed picture for on-street charging). This requires less public investment, and the risks associated with investments being taken by private investors. There is scope for innovation in business models and approaches. As stable and mature business models emerge, over time, provided the market is competitive, prices are likely to align with costs, offering services at efficient levels.

In Scotland, the Scottish government operates a network of public charging points via ChargePlace Scotland, which contracts with site providers (hosts) that have chargepoints in that network located on their property. That requires some public funds to invest, and willingness to take the risks involved in doing so. It brings different trade-offs: government can coordinate deployment (for example, ensuring the number of chargers installed meets the target) and align with other services (like public transport or local government), especially important for on-street deployment. One major difference was that, initially, charging in Scotland was free. This encourages take-up of EVs, but potentially crowds out private investment and creates expectations by consumers that may not be sustained if the policy changes. With its latest strategy, Scotland's approach is now transitioning to a greater role for private sector investment (Endnote 22).

Choices between public or private ownership are political questions, and answered differently in different circumstances. Where there is scope for competition, whether it involves public or private undertakings or both, the CMA can have a role in making those markets work well for consumers. The CMA has made Net Zero a strategic priority and is already active in the sector, so we might expect it to remain vigilant (Endnote 23).

Local government action is critical

Third, it is clear that local government is in the lead in deciding its own strategy for EV charging, supported by money and resources from central government (Endnote 24). This is particularly important for on-street parking, and hence, for urban areas where fewer drivers have room for private off-street charging.

Regulating the electricity network to support decarbonisation

Fourth, I want to touch on the central role played by the energy regulators.

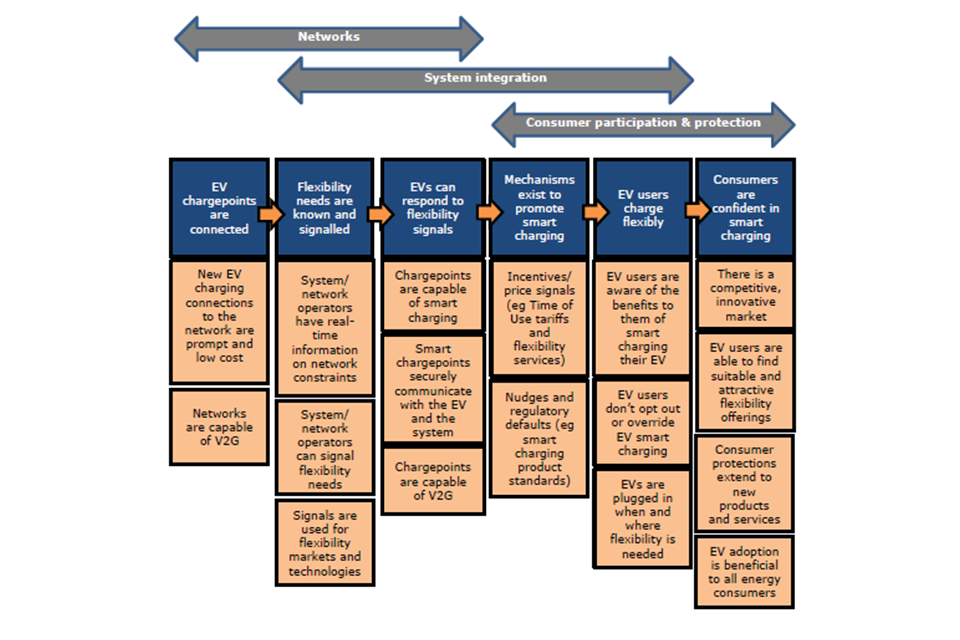

Ofgem, which regulates electricity in Great Britain (but not Northern Ireland) set out its own strategy to support EVs in 2021 - here's the six outcomes and four priorities for its work, as well as the steps needed to deliver those outcomes. (Endnote 25)

Source and