ASIC's review of consumer leases has found evidence of customer harm, with some providers at risk of breaching consumer protection laws. This is despite providers leaving the market following recent reforms.

We reviewed the consumer lease industry to evaluate their implementation of the reforms. We found a significant decline in the number and value of consumer leases, with many providers leaving the sector. Despite these changes in the market, almost 25% of consumer leases are in arrears, indicating the financial vulnerability of many Australians reliant on these arrangements.

Consumer lease providers obtain 80% of their repayments via Centrepay deductions. Proposed reforms to the Centrepay regime include removing consumer leases from it. If these reforms are implemented, more providers are likely to leave the sector.

Within this context, many providers are now moving to alternate credit products that can involve other risks for consumers. We have long held concerns about the detrimental impact of some of these products and will continue to monitor conduct across both the consumer lease and short-term credit markets. Where we consider there to be consumer harm, we will take action to hold providers to account. For example, on 22 May 2025 ASIC took action against Walker Stores for allegedly inflating the cost of household goods, avoiding a rate cap designed to protect consumers, and overcharging interest (25-082MR).

Consumer lease reforms

Consumer leases are contracts that allow a consumer to rent an item for a set period, typically making repayments weekly or fortnightly until the lease ends. What distinguishes a consumer lease from another credit contract is that the provider owns the item at the end of the lease, not the consumer. Consumer leases often impact financially vulnerable and disadvantaged consumers more severely. They have often been provided to Centrelink recipients, with repayments being deducted via Centrepay before a consumer can even access their funds for basic needs such as food.

In December 2022, the Financial Sector Reform Act 2022 introduced reforms to the National Consumer Credit Protection Act 2009 (National Credit Act). These reforms were implemented in response to concerns about harm to consumers due to the practices of consumer lease providers, highlighted in ASIC's work over many years.

Some of the key reforms included:

- a protected earnings regime limiting repayments to no more than 10% of after-tax income

- a cap on costs, limiting the total amount a provider can charge

- an obligation for providers to consider bank statements and document their suitability assessments, and

- anti-avoidance provisions (to prevent consumer lease providers from avoiding the new obligations).

In light of these reforms, we reviewed consumer lease providers to monitor compliance with the new obligations, understand shifts in products made within the sector and identify non-compliance.

We encourage all providers, not just those in our review, to consider the findings and better practices set out in this article. Providers should examine their current policies and procedures for consumer leases to ensure compliance with their legal obligations.

Findings

ASIC's review revealed that:

- several providers have stopped offering consumer leases and some have started to offer alternative regulated credit products, such as sale of goods by instalment and/or lines of credit

- only one of the providers in the review has shown an increase in their consumer lease book. This may be due to other providers ceasing their business and leaving fewer options for consumers to access consumer lease products

- there has been a significant reduction in the number of consumer leases held by customers using Centrepay, the total value of deductions, and deductions exceeding 10% of their after-tax income

- 80% of repayments made to consumer lease providers were made through Centrepay

- there appear to be inconsistent approaches across the industry to the types of fees charged to the contract, resulting in possible breaches of the cap on costs, and

- there appear to be inconsistent and deficient practices among consumer lease providers when it comes to reviewing bank statements and documenting suitability assessments.

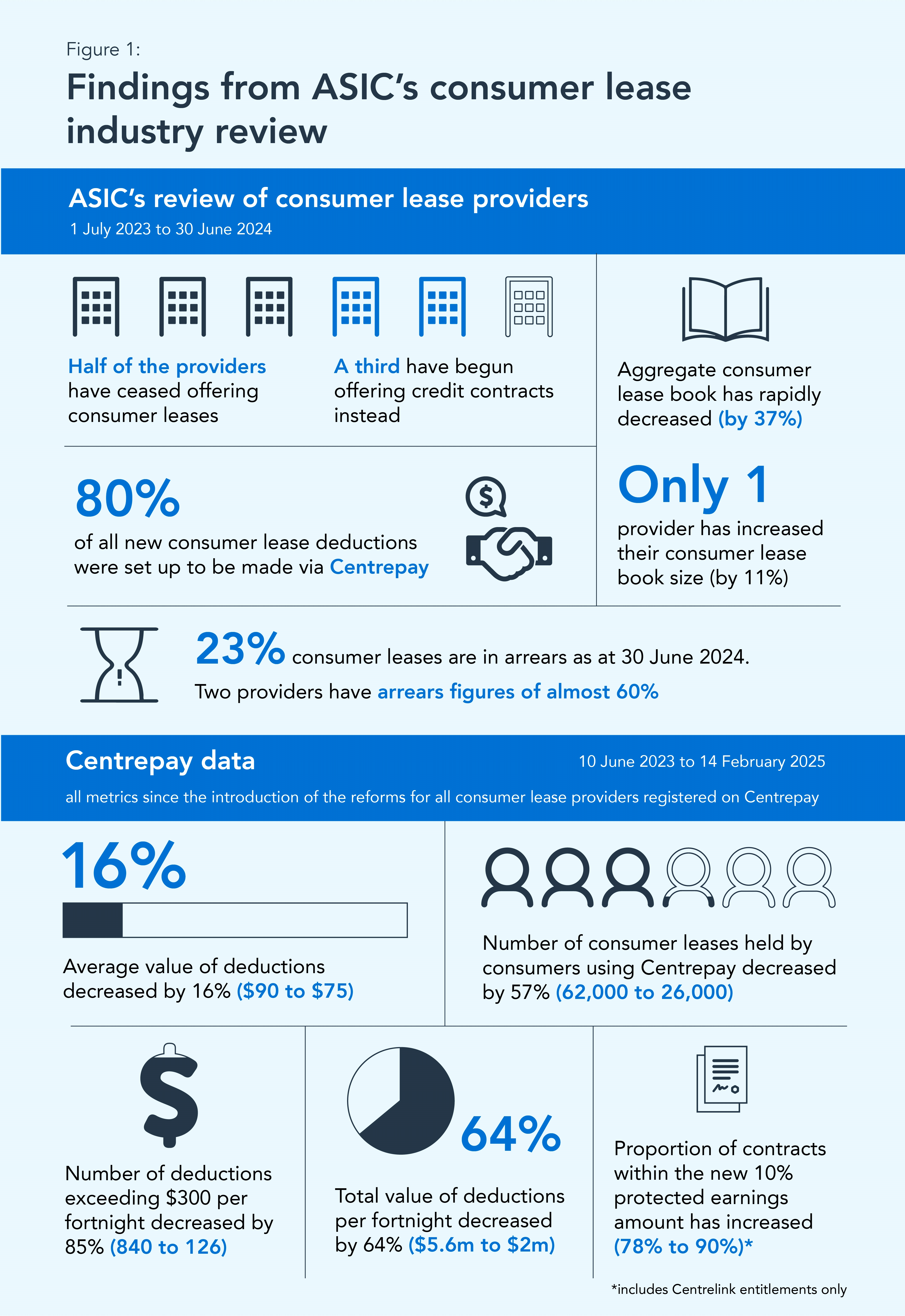

Figure 1 sets out a snapshot of findings from the consumer lease industry review.

Figure 1: Findings from the consumer lease industry review

Figure 1: Findings from the consumer lease industry review - infographic text version

ASIC's review of consumer lease providers: 1 July 2023 to 30 June 2024

- Half of the providers have ceased offering consumer leases

- A third have begun offering credit contracts instead

- Aggregate consumer lease book has rapidly decreased (by 37%)

- Only 1 provider has increased their consumer lease book size (by 11%)

- 80% of all new consumer lease deductions were set up to be made via Centrepay

- 23% of consumer leases are in arrears as at 30 June 2024

- Two providers have arrears figures of almost 60%

Centrepay data: 10 June 2023 to 14 February 2025 (all metrics since the introduction of the reforms for all consumer lease providers registered on Centrepay)

- Average value of deductions decreased by 16% ($90 to $75)

- Number of consumer leases held by consumers using Centrepay decreased by 57% (62,000 to 26,000)

- Number of deductions exceeding $300 per fortnight decreased by 85% (840 to 126)

- Total value of deductions per fortnight decreased by 64% ($5.6m to $2m)

- Proportion of contracts within the new 10% protected earnings amount has increased (78% to 90%)*

*includes Centrelink entitlements only

We observed that there is room for significant improvement in consumer lease providers' compliance with the new obligations, particularly in relation to:

Providers are not doing enough to comply with the protected earnings amount

Under the new obligations, the total rental payments for all consumer leases held by a consumer, including the proposed lease, cannot exceed 10% of a consumer's net income in each payment period: see regulation 28LCB of the National Consumer Credit Regulations 2010 (National Credit Regulations). The protected earnings amount aims to reduce the risk of financially vulnerable consumers being unable to meet their basic needs or default on other necessary commitments as a result of entering into a consumer lease.

Poor practice:

One provider exceeded the protected earnings amount by not considering a consumer's existing consumer lease deductions. The provider had identified the commitment in the Centrelink records held on the consumer's file, but did not appear to have included it in the calculation of the protected earnings amount.

Providers are not identifying whether consumers have existing leases with other providers and are not doing enough to ensure compliance with the protected earnings amount. Most providers are limiting their inquiries to a consumer's Centrelink records and bank statements.

Better practice:

Providers should take all steps necessary to ensure that they have considered existing consumer leases. One provider takes the additional step of reviewing a consumer's credit report and, if they locate a credit inquiry by another provider within the past 12 months, they contact the provider to confirm whether or not the lease is still current. This practice provides greater clarity of commitments and whether the protected earnings amount is being adhered to.

Providers are exceeding the cap on costs

Under the new obligations, a consumer lease provider must not enter into, or vary, a consumer lease so that the total amount payable is more than is allowable under the permitted cap: see section 175AA of the National Credit Code (at Schedule 1 to the National Credit Act). The cap is calculated by adding together the base price of the goods, plus the term (maximum 48 months) multiplied by 0.04, plus any permitted delivery, installation or add-on fees.

Currently, the only permitted fee is a delivery fee, which must be limited to the reasonable cost of delivery. The law allows ASIC to declare by legislative instrument any additional permitted add-on fees or installation fees that can be charged. However, we have not declared any permitted fees to date.

Poor practice:

One provider charged the base price in accordance with regulations, add-on fees for the application process, installation fees, as well as delivery fees that were significantly higher than the supplier delivery fee. This resulted in the cap being breached by the amount of the non-permitted fees. Providers who exceed the permitted cap are in breach of their obligations.

Better practice:

Providers should ensure that the total amount payable does not exceed the permitted cap. We have not made a legislative instrument to declare any permitted installation or add-on fees. Where providers charge delivery fees, they should ensure that the delivery fees are limited to the reasonable costs of delivery of the goods to the consumer.

Providers are not reviewing bank statements adequately or complying with requirements for assessments of suitability

Before entering into a consumer lease, providers must document their preliminary assessment that a lease is not unsuitable for a consumer, together with the inquiries and verification of information. Providers must obtain and review information about each transaction on a consumer's bank statements in undertaking the preliminary assessment: see section 153 of the National Credit Act. Providers must also ensure that they make reasonable inquiries about a consumer's requirements and objectives.

Poor practice:

Three providers obtained bank statements but either did not properly review each transaction or failed to document the inquiries they had undertaken. In one example, the expenses shown in the statement were significantly higher than those used for assessment purposes, which may result in the consumer being committed to a lease that is unaffordable. The providers also failed to record the assessment of the protected earnings amount in the suitability assessment.

In another example, one provider recorded only 'contract is affordable and suitable' in their suitability assessments without any detailed comments as to how this provider reached this conclusion.

Better practice:

Providers must ensure they meet their obligations in assessing consumer bank statements to ensure they are not entering consumers into unsuitable leases. We expect providers to also record the steps taken to inquire and verify the consumer's financial situation, and to record their analysis on why the lease is not unsuitable for the consumer.

Poor practice:

One provider was determining their customer's protected earnings amount and letting them know the maximum lease they could enter, rather than focusing on their customer's objectives. This could lead to a consumer entering into a lease with a higher level of deductions than they otherwise anticipated.

Better practice:

Providers should carefully consider the level of commitment that a consumer is comfortable with, based on the item they want to rent, as opposed to providing the maximum loan on offer. Providers should have clear, well-understood and documented processes in place for verifying and assessing the suitability of a consumer lease.

Providers are not meeting their disclosure obligations

A consumer lease must contain an itemised list of each fee or charge (including any applicable taxes and add-on fees) that forms part of the total amount payable under the consumer lease: see regulation 104A(1) of the National Credit Regulations. The lease must also contain sufficient information to enable the consumer to determine how much they would need to pay to terminate the lease before a fixed-term lease ends.

Poor practice:

One provider did not disclose delivery or add-on fees, or the difference between base price and total amount payable, in the consumer lease agreement. Another provider did not define early termination fees, defining it as 'all costs and expenses incurred in relation to the sale of goods … less all administrative costs in relation to the agreement for the balance of the term'.

Better practice:

Consumer leases must contain the prescribed information at a minimum. Providers should also disclose clearly defined fees that allow the consumer to calculate the amount of fees payable. The definition mentioned above does not contain sufficient information to meet the disclosure obligations prescribed by the reforms.

Providers' hardship practices are not supporting vulnerable consumers

Consumer lease providers should support their customers experiencing financial hardship and make it easy for consumers to give a hardship notice: see section 177B of the National Credit Code.

Poor practice:

One provider's hardship register revealed almost 60% of hardship applications failed to proceed because the provider was waiting for the consumer to provide further information. Consumers whose hardship applications did not proceed included those who stated they were experiencing domestic violence or mental health issues.

Better practice:

A significantly high failure rate should signal to consumer lease providers that they need to review their process. Making it easy for consumers to give a hardship notice increases their chances of financial recovery: see Report 782 Hardship, hard to get help: Findings and actions to support customers in financial hardship (REP 782) and Report 783 Hardship, hard to get help: Lenders fall short in financial hardship support (REP 783).

Providers are leaving the consumer leasing sector in favour of offering alternate credit contracts

The reforms include a new anti-avoidance provision: see section 323A of the National Credit Act. This prohibits a person from entering into or carrying out a scheme for an avoidance purpose in relation to consumer leases. An avoidance purpose is broadly defined and includes conduct that prevents a contract from being a consumer lease.

We have observed a significant shift away from providers offering consumer leases and into other credit products. For example, some providers are now offering sale of goods by instalment contracts and lines of credit to buy household goods.

We are reviewing these products and the pricing policies providers are adopting. We aim to determine whether this shift by providers into other credit products is seeking to avoid the additional consumer protections imposed on consumer leases, and whether there is any evidence of consumer harm.

Other developments

Centrepay reform

In December 2024, the Australian Government announced a range of improvements to Centrepay to ensure the free bill paying service helps Australians and reduces the risk of financial harm.

As part of the proposed reforms, Centrepay will be improved by removing high-risk services, including consumer leases and household goods, to realign Centrepay as a regular bill-paying service that reduces financial risk.

Given the heavy reliance by consumer lease providers on Centrepay to obtain their repayments, these proposed reforms may result in a further contraction in the size of the consumer lease market.

ASIC enforcement action

On 22 May 2025 ASIC commenced proceedings against Walker Stores Pty Ltd (trading as Snaffle)(25-082MR). We allege that they have exceeded the 48% annual cost rate cap, calculated interest on an unlawful basis (which resulted in Snaffle charging excessive interest) and failed to disclose key information in their credit contracts. All these provisions are designed to protect consumers from potentially exploitative lending practices.

We will continue to monitor compliance from consumer lease providers, along with any further moves to alternate credit product offerings. We are considering our regulatory options in relation to these movements and will take enforcement action where appropriate.

Review methodology

To review the consumer lease industry, we:

- met with key stakeholders (consumer advocates, industry representatives and consumer lease providers)

- obtained Centrepay data from Services Australia, with metrics focused on movements in deductions

- reviewed internal intelligence and data we held

- issued notices on six providers (which includes all locations and franchisees) seeking a limited set of qualitative and quantitative information. This information included:

- metrics regarding consumer leases and other credit products, including terms, annual cost rates and cost caps, number of applications, and contract value. The metrics related to the period between 1 January 2023 and 30 June 2024

- a selection of consumer files, including suitability assessments, and

- policies and procedures documenting pricing practices, fees and adherence to the new obligations, and

- conducted a desktop website review of 12 providers.

Background

The review on consumer leases is part of ASIC's continued focus on the sector:

- We have taken several enforcement actions over the years against consumer lease providers and providers of sale of goods by instalment credit contracts:

- In September 2024, the Federal Court found that Rent4Keeps and one of its franchises attempted to style their lending arrangements as consumer leases - however, they were credit contracts and contravened the 48% annual rate cap and other obligations under the National Credit Act (see 24-195MR).

- In June 2023, the Federal Court ordered Layaway Depot Pty Ltd pay a penalty of $375,000 for breaches of the National Credit Act (see 23-139MR). Layaway charged excessive interest rates on 70 loans taken out by consumers to buy electronic goods.

- In April 2021, the Federal Court ordered GoGetta Equipment Funding Pty Ltd to pay a $750,000 penalty for engaging in unlicensed consumer leasing (see 21-086MR).

- In November 2018, we issued $157,500 in fines and accepted a court enforceable undertaking following concerns that Local Appliance Rentals Pty Ltd failed to meet its responsible lending obligations, received excess payments from consumers in relation to their lease and charged excess late fees, and failed to adequately supervise its franchisees (see 18-337MR).

- In May 2018, the Federal Court ordered Thorn Australia Pty Ltd's Radio Rentals for contravening responsible lending obligations (see 18-139MR). The court found that Thorn failed to make the necessary inquiries and take steps to verify the financial situation of its customers, and failed to conduct a proper assessment of the suitability of the leases it provided.

- We published Report 447 Cost of consumer leases for household goods (REP 447) in 2015, which found that:

- different providers charged significantly different amounts for the same goods, known as price dispersion, and

- the same provider would charge significantly different amounts for the same goods for different consumer segments, known as price discrimination.

/Public Release. This material from the originating organization/author(s) might be of the point-in-time nature, and edited for clarity, style and length. Mirage.News does not take institutional positions or sides, and all views, positions, and conclusions expressed herein are solely those of the author(s).View in full

here.