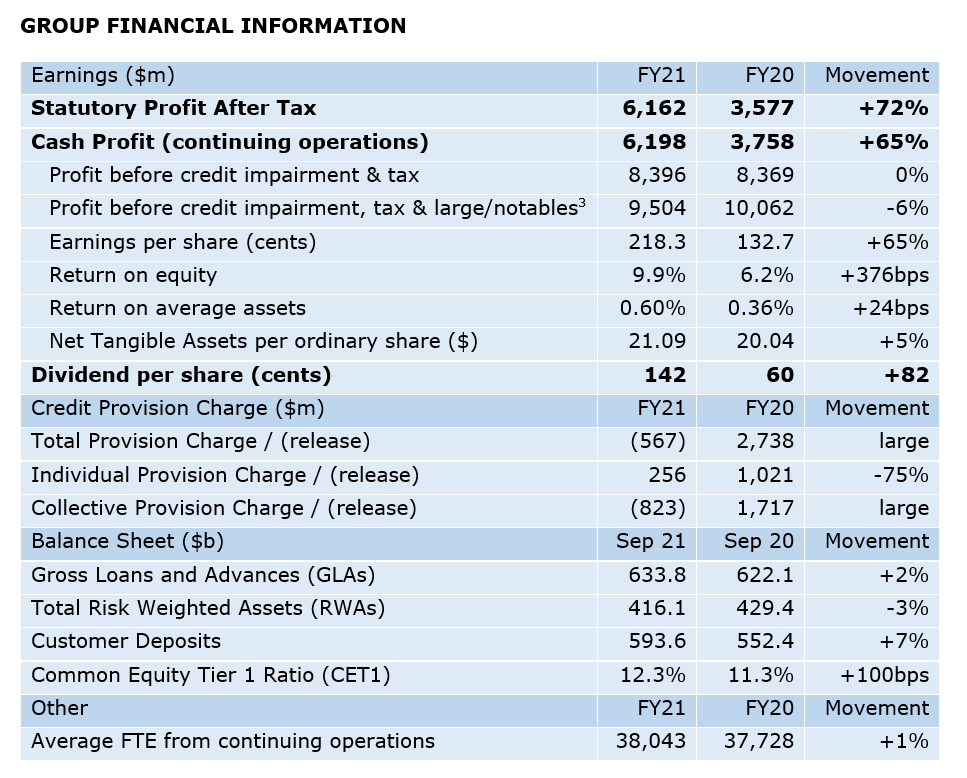

ANZ today announced an audited[1] Statutory Profit after tax for the year ended 30 September 2021 of $6,162 million, up 72% on the prior year with a key driver being the partial reversal of COVID-19 related credit provisions.

Cash Profit[2] from continuing operations, before credit impairment and tax, was $8,396 million, flat to the prior year.

ANZ's Common Equity Tier 1 Ratio was stronger at 12.3% while Cash Return on Equity increased to 9.9%.

- Profits grew in Australia Retail & Commercial despite challenges in home loans processing

- New Zealand had one of its strongest years with solid balance sheet momentum

- Consistent performance in Institutional with returns again well above the Group cost of capital

- Expenses tightly managed while increasing investment

- Capital managed prudently

ANZ Chief Executive Officer Shayne Elliott said: "This year demonstrated the benefits of our diversified portfolio as we provided solid returns for shareholders while also successfully navigating the continuing impacts of COVID-19 on our customers and our people.

"Australia Retail & Commercial grew lending and customer deposits during the year and delivered good margin performance across the division. Home loan revenue growth was in the low double digits. However, second half volumes were impacted by a competitive refinancing market, customers paying down their loans faster and processing issues. We have been working on a range of improvements and they are already having a positive impact on processing times.

"A focus on improving customer outcomes as well as realising the benefits of prior investments helped New Zealand deliver one of its strongest performances ever. Home loans grew 11% while still taking proactive steps to bring balance to the housing market, such as lifting the deposit required for investor lending. We also maintained our position as the largest provider of KiwiSaver, growing funds under management by 16% to NZ$19 billion.

"Institutional delivered another consistent performance, reflecting the benefits of a simpler, more diversified franchise. This is a business providing sustainable returns well above the Group cost of capital. Markets revenue just below $2 billion in the current environment is testament to its strength and diversity as well as prudent risk settings.

"Our progress in simplifying the business drove down the cost of running the bank for the third consecutive year and we continue to invest in new initiatives at record pace to build a stronger base for future growth. We also managed shareholder capital prudently and led the industry in returning funds to shareholders.

"While we benefitted from a more benign credit environment, indicators such as 90+ days past due and deferrals performed better than expected and reflected our prudent management over many years. We recognise the outlook remains somewhat uncertain and we have more than $4 billion of credit reserves should conditions deteriorate.

"We managed our business against the backdrop of COVID-19. Our employee engagement remained at historically high levels, even as staff largely worked remotely, and we supported our customers in need through the reinstatement of loan deferrals as well as providing finance to increase economic activity," Mr Elliott said.

DIVIDEND & CAPITAL

Capital management remained a feature with ANZ's Common Equity Tier 1 Ratio of 12.3%, remaining ~$6 billion[5] above Australian Prudential Regulation Authority's 'Unquestionably Strong' benchmark. Combined with solid earnings and improving conditions, the Board determined a Final Dividend of 72 cents per share (cps) was appropriate, taking the Total Dividend for 2021 to 142cps, up by 82cps on the prior year.

In August 2021, ANZ commenced a buy-back of $1.5 billion shares on-market. This reflected our ability to continue to support our customers while also returning surplus capital in a prudent, fair and flexible manner. As at 30 September 2021, ANZ is almost half-way through its current $1.5 billion buyback and will continue to consider the best use of any surplus capital.

ANZ also announced the Dividend Reinvestment Plan (DRP) will continue to apply for the Final 2021 Dividend at no discount and that it plans to neutralise the impact of the shares allocated under the DRP.

CREDIT QUALITY

The total provision result for the full year was a net release of $567 million comprising:

- a collective provision (CP) release of $823 million

- an individually assessed provision (IP) charge of $256 million

The CP release is due to a combination of factors, with changes to the portfolio volume, mix and risk profile occurring throughout the year, and the economic outlook improving in the first half. As at 30 September 2021, the uncertainty arising from extended lockdowns in major cities has limited further such releases in the second half.

In general, our customers continued to manage well through the pandemic, leading to a low IP charge for the full year. Disciplined focus on strategy and customer selection in Institutional has contributed to this strong result, as has the continued impact of government and bank support packages. At the end of the financial year, the CP balance of $4,195 million represents additional provisions of $819 million compared with pre-COVID levels at 30 September 2019.

OPERATIONAL HIGHLIGHTS

Australia Retail & Commercial

- Applications for our automated business lending proposition, ANZ GoBiz, have averaged 2,900 per-month since launching in May 2021. GoBiz provides real-time conditional approval through an on-line platform, including new-to-bank customers.

- Provided 179,000 new home loan accounts in Australia, up 5% from FY20.

- 49% of all retail sales in Australia, including home loans, are now through digital channels, up from 40% in FY20.

New Zealand

- Maintained market leadership in core product sectors; home loans grew by almost ~NZ$10b or 11% with a record ~82,000 new home loan accounts processed and 178,000 existing customers re-fixing their home loans during the year.

- Remains the largest KiwiSaver provider with NZ$19 billion under management, an increase of NZ$2.6 billion or 16% on the previous year.

- 41% of all retail sales in New Zealand, including home loans, are now through digital channels, up from 38% in FY20.

Institutional

- 24% increase in the volume of payments made by our customers through our digital payments platform.

- Disciplined expense management with the division achieving 11 consecutive halves of absolute cost reduction.

- Transactions processed by ANZ on the New Payments Platform for other banks increased 112% year-on-year.

- Revenue from our Sustainable Finance business up 63% year-on-year; also ranked #1 Market Leader in ESG finance in Australia and New Zealand[6], as well as launching a new Sustainability-Linked Derivative product across our franchise.

- New savings and deposits proposition being developed as part of ANZx moved to Beta phase with successful launch of a staff trial.

- Separation of ventures and incubator business, 1835i, to create a stand-alone entity to accelerate growth and deliver new digital solutions.

- Strong progress on open banking obligations as a CDR Data Holder and on track to commence data sharing for businesses customers on 1 November 2021.